AMZN--

AVGO--

META--

MSFT--

NVDA--

avgo broadcom moat analysis ai chips

Everyone is debating whether to buy AVGO on the dip. Most of them are asking the wrong question.

The right question isn't "is AVGO cheap at $430?" It's "is the custom silicon moat still intact — and who is most likely to erode it?"

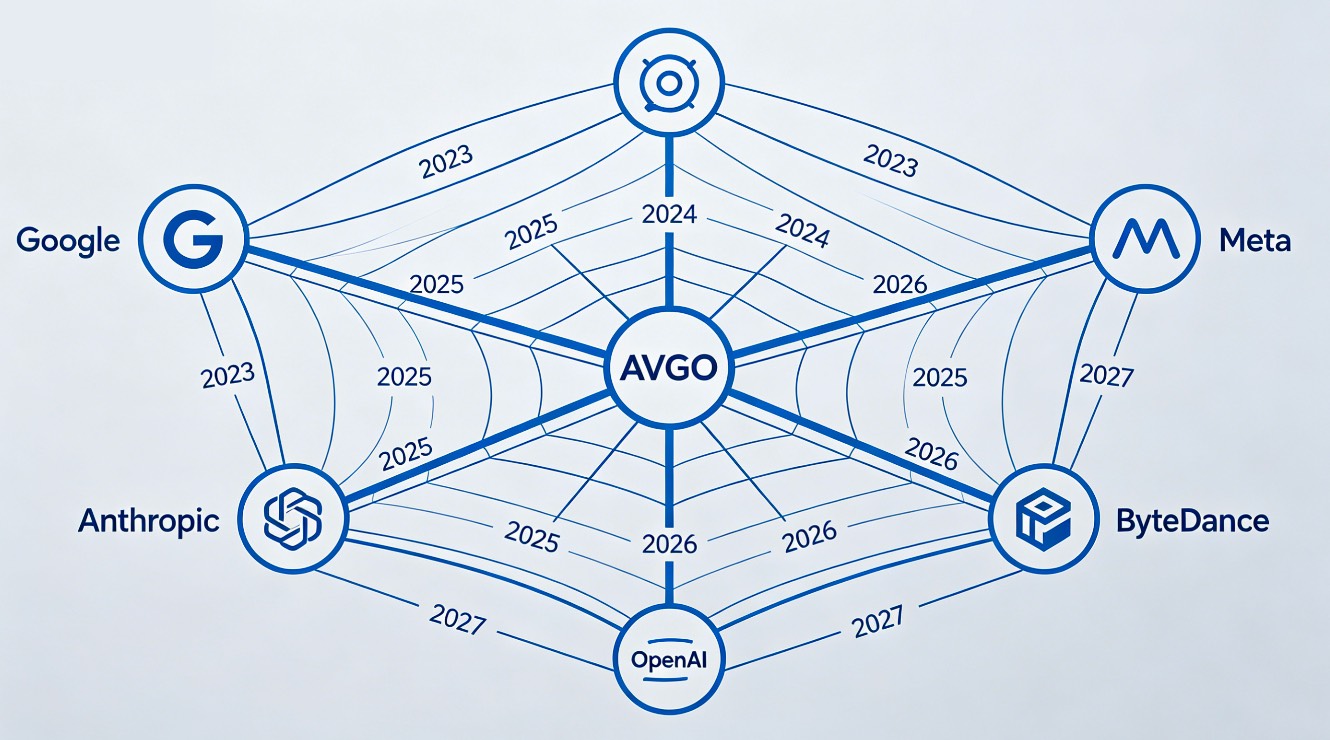

Let's be precise about the moat. Broadcom's business model is fundamentally different from Nvidia's. Nvidia sells the same H100/B200 to everyone. Broadcom co-designs a unique XPU for each hyperscaler client — Google's TPU, Meta's MTIA, ByteDance's internal silicon, and now chips for Anthropic and OpenAI. Each design takes 18–24 months of co-engineering. Once the chip is in production, the customer can't switch without losing 2 years of development time and rebuilding from scratch. That's an extraordinarily high switching cost.

The moat is real. But it has three genuine vulnerabilities.

First: insourcing risk. Amazon already moved Trainium 3 fully in-house. Microsoft is deepening Maia 2 without Broadcom involvement. If Meta or Google decides to follow AWS and build its own networking + accelerator stack entirely, Broadcom loses a customer representing 15–20% of revenue with no replacement pipeline.

Second: concentration. Five customers represent roughly 50% of Broadcom's semiconductor revenue. That's not a diversified business — it's a concentrated bet on the continued AI capex commitments of five specific companies. If any one of them hits a capex cycle pause, the impact is immediate and disproportionate.

Third: the software miss this week. Infrastructure software — the VMware/enterprise stack — came in $140M light. That's 0.6% of revenue. But the trend matters more than the number. If software is plateauing while AI chips soar, the "AI + software compounding" re-rating thesis loses one of its two legs.

The bull case survives all three of these risks — for now. Google's supply agreement runs through 2031. Meta's MTIA roadmap still relies on Broadcom networking even if compute moves in-house. Anthropic and OpenAI are new customers adding to the revenue base. And the Q3 guide of $16B at 200% YoY growth is, by any measure, extraordinary.

But at 87x earnings, "survives the risks" isn't enough. You need "dominates despite the risks." That's a different standard. And that's why today's NFP — and whether it gives AVGO a multiple-expansion tailwind from rate relief — matters as much as the fundamental story.

The right question isn't "is AVGO cheap at $430?" It's "is the custom silicon moat still intact — and who is most likely to erode it?"

Let's be precise about the moat. Broadcom's business model is fundamentally different from Nvidia's. Nvidia sells the same H100/B200 to everyone. Broadcom co-designs a unique XPU for each hyperscaler client — Google's TPU, Meta's MTIA, ByteDance's internal silicon, and now chips for Anthropic and OpenAI. Each design takes 18–24 months of co-engineering. Once the chip is in production, the customer can't switch without losing 2 years of development time and rebuilding from scratch. That's an extraordinarily high switching cost.

The moat is real. But it has three genuine vulnerabilities.

First: insourcing risk. Amazon already moved Trainium 3 fully in-house. Microsoft is deepening Maia 2 without Broadcom involvement. If Meta or Google decides to follow AWS and build its own networking + accelerator stack entirely, Broadcom loses a customer representing 15–20% of revenue with no replacement pipeline.

Second: concentration. Five customers represent roughly 50% of Broadcom's semiconductor revenue. That's not a diversified business — it's a concentrated bet on the continued AI capex commitments of five specific companies. If any one of them hits a capex cycle pause, the impact is immediate and disproportionate.

Third: the software miss this week. Infrastructure software — the VMware/enterprise stack — came in $140M light. That's 0.6% of revenue. But the trend matters more than the number. If software is plateauing while AI chips soar, the "AI + software compounding" re-rating thesis loses one of its two legs.

The bull case survives all three of these risks — for now. Google's supply agreement runs through 2031. Meta's MTIA roadmap still relies on Broadcom networking even if compute moves in-house. Anthropic and OpenAI are new customers adding to the revenue base. And the Q3 guide of $16B at 200% YoY growth is, by any measure, extraordinary.

But at 87x earnings, "survives the risks" isn't enough. You need "dominates despite the risks." That's a different standard. And that's why today's NFP — and whether it gives AVGO a multiple-expansion tailwind from rate relief — matters as much as the fundamental story.

Disclaimer: The above is a summary showing certain market information. Ainvest is not responsible for any data errors, omissions or other information that may be displayed incorrectly as the data is derived from a third party source. Communications displaying market prices, data and other information available in this post are meant for informational purposes only and are not intended as an offer or solicitation for the purchase or sale of any security. Please do your own research when investing, All investments involve risk and the past performance of a security, or financial product does not guarantee future results or returns. Keep in mind that while diversification may help spread risk it does not assure a profit, or protect against loss, in a down market.Report an Issue

CONTACT US

Email: support@ainvest.com

Address: 330 7th Ave, Suite 902, New York, NY 10001, US

Copyright 2026 AInvest Fintech Inc. All rights reserved.

Comments

No comments yet