minesskiier 06/05

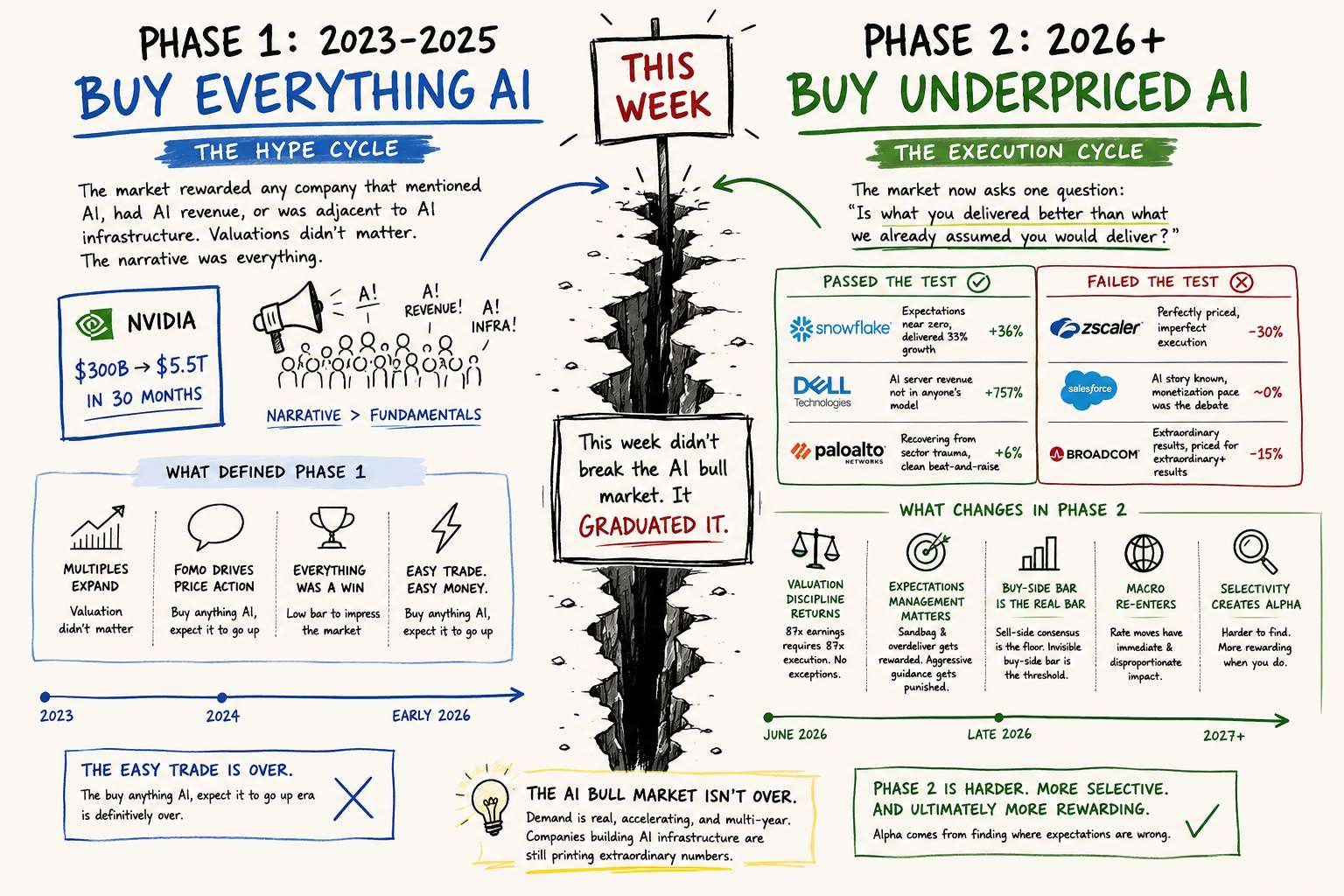

This week didn't break the AI bull market. It graduated it.Phase 1 (2023–early 2026): The AI hype cycle. The market rewarded any company that mentioned AI, had AI revenue, or was adjacent to AI infrastructure. Valuations didn't matter. The narrative was everything. Nvidia going from $300B to $5.5T in 30 months is the defining data point of Phase 1.

Phase 2 (June 2026 onward): The execution cycle. Phase 1 ended not with a crash, but with a repricing. The market spent this week systematically repricing every major AI name based on one question: "Is what you delivered better than what we already assumed you would deliver?"

The companies that passed Phase 2's test: Snowflake (expectations near zero, delivered 33% growth), Dell (AI server revenue literally not in anyone's model at 757%), PANW (recovering from sector trauma, clean beat-and-raise).

The companies that failed Phase 2's test: Zscaler (perfectly priced, imperfect execution), Salesforce (AI story known, monetization pace was the debate), Broadcom (extraordinary results, but priced for extraordinary+ results).

What changes in Phase 2:

Valuation discipline returns. 87x earnings requires 87x execution. No exceptions.

Expectations management becomes a competitive advantage. The companies that sandbag guidance and overdeliver will be rewarded. The ones that set aggressive guidance will be punished on any shortfall.

The buy-side bar replaces earnings beats as the primary signal. Sell-side consensus is the floor. The invisible buy-side bar is the real threshold.

Macro re-enters the equation. In Phase 1, rate uncertainty was an inconvenience. In Phase 2, with multiples still extended, rate moves have immediate and disproportionate impact on stock prices.

The AI bull market isn't over. The companies building AI infrastructure are still printing extraordinary numbers. The demand is real, accelerating, and multi-year. But the easy trade — buy anything AI, expect it to go up — is definitively over.

Phase 2 is harder, more selective, and ultimately more rewarding for investors who do the work to find where expectations are wrong.

Welcome to the real AI trade.

SNOW--

DELL--

PANW--

ZS--

CRM--

AVGO--

NVDA--

SNOW--

DELL--

PANW--

ZS--

CRM--

AVGO--

Sensitive-Fix8857 06/05

Feels like Phase 2 starts now. I’m watching SNOW and DELL for execution clarity before adding to my AI sleeve.

Wheremytendies 06/05

The math checks out: SNOW at 33% growth while expectations were near zero, DELL with 757% AI server revenue, PANW recovering. If multiples are disciplined, 87x requires consistency. I’m favoring SNOW and DELL over ZS and CRM until execution proves itself.

stakeandshake 06/05

Hard to buy the narrative without context: SNOW at 20x with 33% growth feels fine, but CRM at 30x with 10–15% is stretched. If hyperscaler AI budgets normalize, software multiples compress fast.

Scroll to load more

Gesetz

DatenschutzerklärungNutzungsbedingungenAIME NutzungsbedingungenHaftungsausschluss für MaklerOffenlegung von Risiken durch künstliche IntelligenzKontaktieren Sie uns

Email: support@ainvest.com

Address: 330 7th Ave, Suite 902, New York, NY 10001, US

Copyright 2026 AInvest Fintech Inc. All rights reserved.