June 3 Daily Discussion: Is Broadcom About to Make or Break the AI Rally?

15.0KViews

0Posts

What matters most tonight?

Broadcom Beats Again

AI Spending Slows

45%

55%

487

Votes

Vote closed

View post details

Everyone is debating whether to buy AVGO on the dip. Most of them are asking the wrong question.

The right question isn't "is AVGO cheap at $430?" It's "is the custom silicon moat still intact — and who is most likely to erode it?"

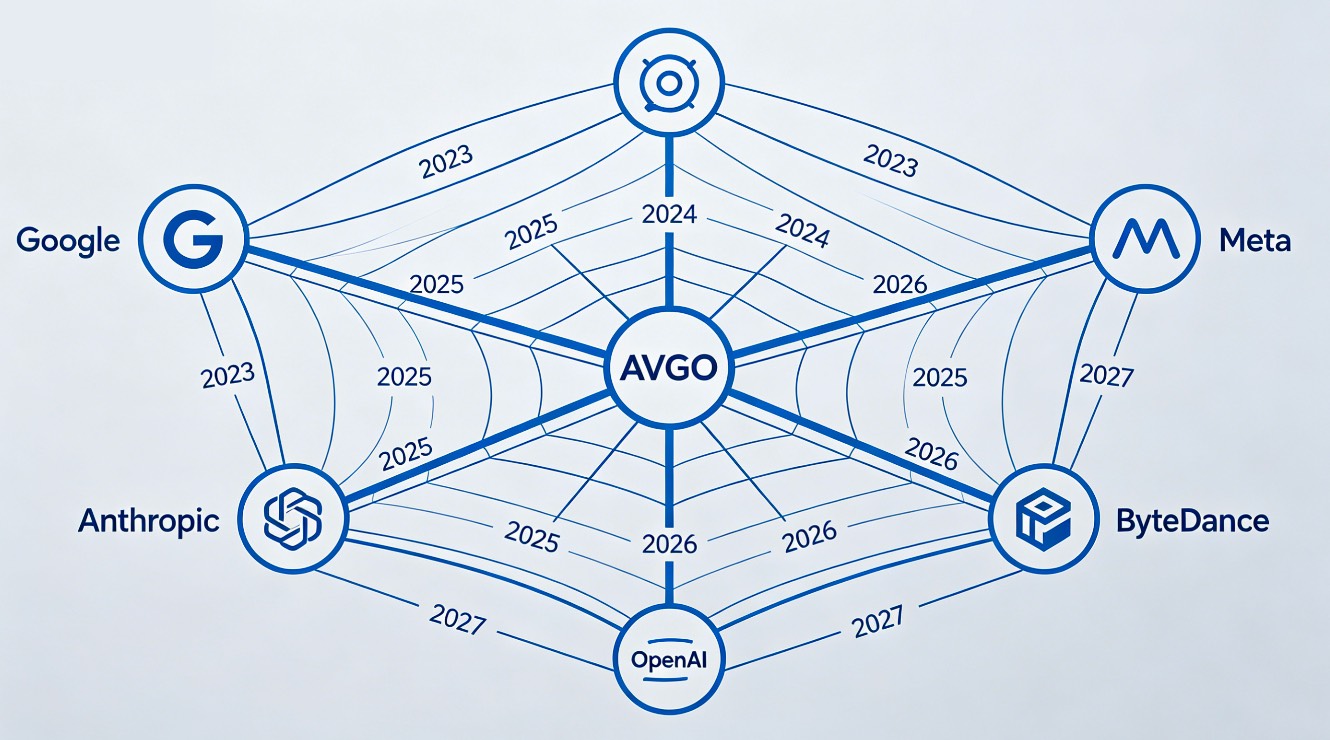

Let's be precise about the moat. Broadcom's business model is fundamentally different from Nvidia's. Nvidia sells the same H100/B200 to everyone. Broadcom co-designs a unique XPU for each hyperscaler client — Google's TPU, Meta's MTIA, ByteDance's internal silicon, and now chips for Anthropic and OpenAI. Each design takes 18–24 months of co-engineering. Once the chip is in production, the customer can't switch without losing 2 years of development time and rebuilding from scratch. That's an extraordinarily high switching cost.

The moat is real. But it has three genuine vulnerabilities.

First: insourcing risk. Amazon already moved Trainium 3 fully in-house. Microsoft is deepening Maia 2 without Broadcom involvement. If Meta or Google decides to follow AWS and build its own networking + accelerator stack entirely, Broadcom loses a customer representing 15–20% of revenue with no replacement pipeline.

Second: concentration. Five customers represent roughly 50% of Broadcom's semiconductor revenue. That's not a diversified business — it's a concentrated bet on the continued AI capex commitments of five specific companies. If any one of them hits a capex cycle pause, the impact is immediate and disproportionate.

Third: the software miss this week. Infrastructure software — the VMware/enterprise stack — came in $140M light. That's 0.6% of revenue. But the trend matters more than the number. If software is plateauing while AI chips soar, the "AI + software compounding" re-rating thesis loses one of its two legs.

The bull case survives all three of these risks — for now. Google's supply agreement runs through 2031. Meta's MTIA roadmap still relies on Broadcom networking even if compute moves in-house. Anthropic and OpenAI are new customers adding to the revenue base. And the Q3 guide of $16B at 200% YoY growth is, by any measure, extraordinary.

But at 87x earnings, "survives the risks" isn't enough. You need "dominates despite the risks." That's a different standard. And that's why today's NFP — and whether it gives AVGO a multiple-expansion tailwind from rate relief — matters as much as the fundamental story.

The right question isn't "is AVGO cheap at $430?" It's "is the custom silicon moat still intact — and who is most likely to erode it?"

Let's be precise about the moat. Broadcom's business model is fundamentally different from Nvidia's. Nvidia sells the same H100/B200 to everyone. Broadcom co-designs a unique XPU for each hyperscaler client — Google's TPU, Meta's MTIA, ByteDance's internal silicon, and now chips for Anthropic and OpenAI. Each design takes 18–24 months of co-engineering. Once the chip is in production, the customer can't switch without losing 2 years of development time and rebuilding from scratch. That's an extraordinarily high switching cost.

The moat is real. But it has three genuine vulnerabilities.

First: insourcing risk. Amazon already moved Trainium 3 fully in-house. Microsoft is deepening Maia 2 without Broadcom involvement. If Meta or Google decides to follow AWS and build its own networking + accelerator stack entirely, Broadcom loses a customer representing 15–20% of revenue with no replacement pipeline.

Second: concentration. Five customers represent roughly 50% of Broadcom's semiconductor revenue. That's not a diversified business — it's a concentrated bet on the continued AI capex commitments of five specific companies. If any one of them hits a capex cycle pause, the impact is immediate and disproportionate.

Third: the software miss this week. Infrastructure software — the VMware/enterprise stack — came in $140M light. That's 0.6% of revenue. But the trend matters more than the number. If software is plateauing while AI chips soar, the "AI + software compounding" re-rating thesis loses one of its two legs.

The bull case survives all three of these risks — for now. Google's supply agreement runs through 2031. Meta's MTIA roadmap still relies on Broadcom networking even if compute moves in-house. Anthropic and OpenAI are new customers adding to the revenue base. And the Q3 guide of $16B at 200% YoY growth is, by any measure, extraordinary.

But at 87x earnings, "survives the risks" isn't enough. You need "dominates despite the risks." That's a different standard. And that's why today's NFP — and whether it gives AVGO a multiple-expansion tailwind from rate relief — matters as much as the fundamental story.

70

20

8

Empty_Somewhere_2135:Volatility like this is where I park cash and watch AVGO. If NFP softens and rates ease, I’ll nibble on dips, but I’m hedging with a small NVDA collar. The moat’s there, just not bulletproof.

car12703:The multiple here is hostage to the labor market and rates. If NFP stays soft into summer, the Fed might pause, and AVGO could get a tailwind. But if capex slows, even a 10% drop in hyperscaler spend hits margins fast.

See all comments

View post details

Here's the macro risk that's hiding in plain sight behind today's NFP narrative.

The entire AI bull market of May 2026 was built on a four-part thesis: AI demand is real and accelerating; inflation is cooling because oil is falling; the Fed will eventually cut; therefore, high-multiple tech is justified.

Three of those four pillars are now wobbling simultaneously.

Oil: WTI was at $88–90 two weeks ago. It's back near $92–93. Iran talks are suspended. Trump says a "final determination" is coming. Goldman's adverse scenario — Brent at $115 if Hormuz reopens slowly — is back on the table. A $20 oil shock from here re-ignites the inflation story that was supposed to be over.

Inflation: PCE at 3.8%, PPI at 6.0%. The "cooling" narrative was always dependent on oil staying suppressed. If oil re-accelerates, the disinflation story reverses.

The Fed: Markets are pricing a near-certain hold. But a hawkish hold — "we see upside risks to inflation" — is a completely different signal than a dovish hold. Warsh inherits a press conference in 12 days where one wrong sentence re-prices the entire rate curve.

The fourth pillar — AI demand — remains intact. Dell's $24.4B in orders, Broadcom's $10.8B AI revenue, Snowflake's reacceleration, all confirm it.

But here's the danger: three wobbling pillars with one strong one isn't a stable structure. It's a building held up by its strongest wall while the other three crack. The AI demand story can carry the market for a while. It can't carry it forever if rates stay higher-for-longer and oil re-accelerates.

Watch oil this weekend. Not earnings. Not NFP. Oil.

Here's the macro risk that's hiding in plain sight behind today's NFP narrative.

The entire AI bull market of May 2026 was built on a four-part thesis: AI demand is real and accelerating; inflation is cooling because oil is falling; the Fed will eventually cut; therefore, high-multiple tech is justified.

Three of those four pillars are now wobbling simultaneously.

Oil: WTI was at $88–90 two weeks ago. It's back near $92–93. Iran talks are suspended. Trump says a "final determination" is coming. Goldman's adverse scenario — Brent at $115 if Hormuz reopens slowly — is back on the table. A $20 oil shock from here re-ignites the inflation story that was supposed to be over.

Inflation: PCE at 3.8%, PPI at 6.0%. The "cooling" narrative was always dependent on oil staying suppressed. If oil re-accelerates, the disinflation story reverses.

The Fed: Markets are pricing a near-certain hold. But a hawkish hold — "we see upside risks to inflation" — is a completely different signal than a dovish hold. Warsh inherits a press conference in 12 days where one wrong sentence re-prices the entire rate curve.

The fourth pillar — AI demand — remains intact. Dell's $24.4B in orders, Broadcom's $10.8B AI revenue, Snowflake's reacceleration, all confirm it.

But here's the danger: three wobbling pillars with one strong one isn't a stable structure. It's a building held up by its strongest wall while the other three crack. The AI demand story can carry the market for a while. It can't carry it forever if rates stay higher-for-longer and oil re-accelerates.

Watch oil this weekend. Not earnings. Not NFP. Oil.

The entire AI bull market of May 2026 was built on a four-part thesis: AI demand is real and accelerating; inflation is cooling because oil is falling; the Fed will eventually cut; therefore, high-multiple tech is justified.

Three of those four pillars are now wobbling simultaneously.

Oil: WTI was at $88–90 two weeks ago. It's back near $92–93. Iran talks are suspended. Trump says a "final determination" is coming. Goldman's adverse scenario — Brent at $115 if Hormuz reopens slowly — is back on the table. A $20 oil shock from here re-ignites the inflation story that was supposed to be over.

Inflation: PCE at 3.8%, PPI at 6.0%. The "cooling" narrative was always dependent on oil staying suppressed. If oil re-accelerates, the disinflation story reverses.

The Fed: Markets are pricing a near-certain hold. But a hawkish hold — "we see upside risks to inflation" — is a completely different signal than a dovish hold. Warsh inherits a press conference in 12 days where one wrong sentence re-prices the entire rate curve.

The fourth pillar — AI demand — remains intact. Dell's $24.4B in orders, Broadcom's $10.8B AI revenue, Snowflake's reacceleration, all confirm it.

But here's the danger: three wobbling pillars with one strong one isn't a stable structure. It's a building held up by its strongest wall while the other three crack. The AI demand story can carry the market for a while. It can't carry it forever if rates stay higher-for-longer and oil re-accelerates.

Watch oil this weekend. Not earnings. Not NFP. Oil.

Here's the macro risk that's hiding in plain sight behind today's NFP narrative.

The entire AI bull market of May 2026 was built on a four-part thesis: AI demand is real and accelerating; inflation is cooling because oil is falling; the Fed will eventually cut; therefore, high-multiple tech is justified.

Three of those four pillars are now wobbling simultaneously.

Oil: WTI was at $88–90 two weeks ago. It's back near $92–93. Iran talks are suspended. Trump says a "final determination" is coming. Goldman's adverse scenario — Brent at $115 if Hormuz reopens slowly — is back on the table. A $20 oil shock from here re-ignites the inflation story that was supposed to be over.

Inflation: PCE at 3.8%, PPI at 6.0%. The "cooling" narrative was always dependent on oil staying suppressed. If oil re-accelerates, the disinflation story reverses.

The Fed: Markets are pricing a near-certain hold. But a hawkish hold — "we see upside risks to inflation" — is a completely different signal than a dovish hold. Warsh inherits a press conference in 12 days where one wrong sentence re-prices the entire rate curve.

The fourth pillar — AI demand — remains intact. Dell's $24.4B in orders, Broadcom's $10.8B AI revenue, Snowflake's reacceleration, all confirm it.

But here's the danger: three wobbling pillars with one strong one isn't a stable structure. It's a building held up by its strongest wall while the other three crack. The AI demand story can carry the market for a while. It can't carry it forever if rates stay higher-for-longer and oil re-accelerates.

Watch oil this weekend. Not earnings. Not NFP. Oil.

71

21

4

IndividualistAW:If Brent hits $115, does the Fed pivot faster?

eujc21:This whole setup feels fragile. One oil headline, one Fed tone, and the market swings. I’m uneasy riding this AI wave if the backdrop keeps wobbling. I’d rather see a cleaner disinflation story before getting emotional.

See all comments

View post details

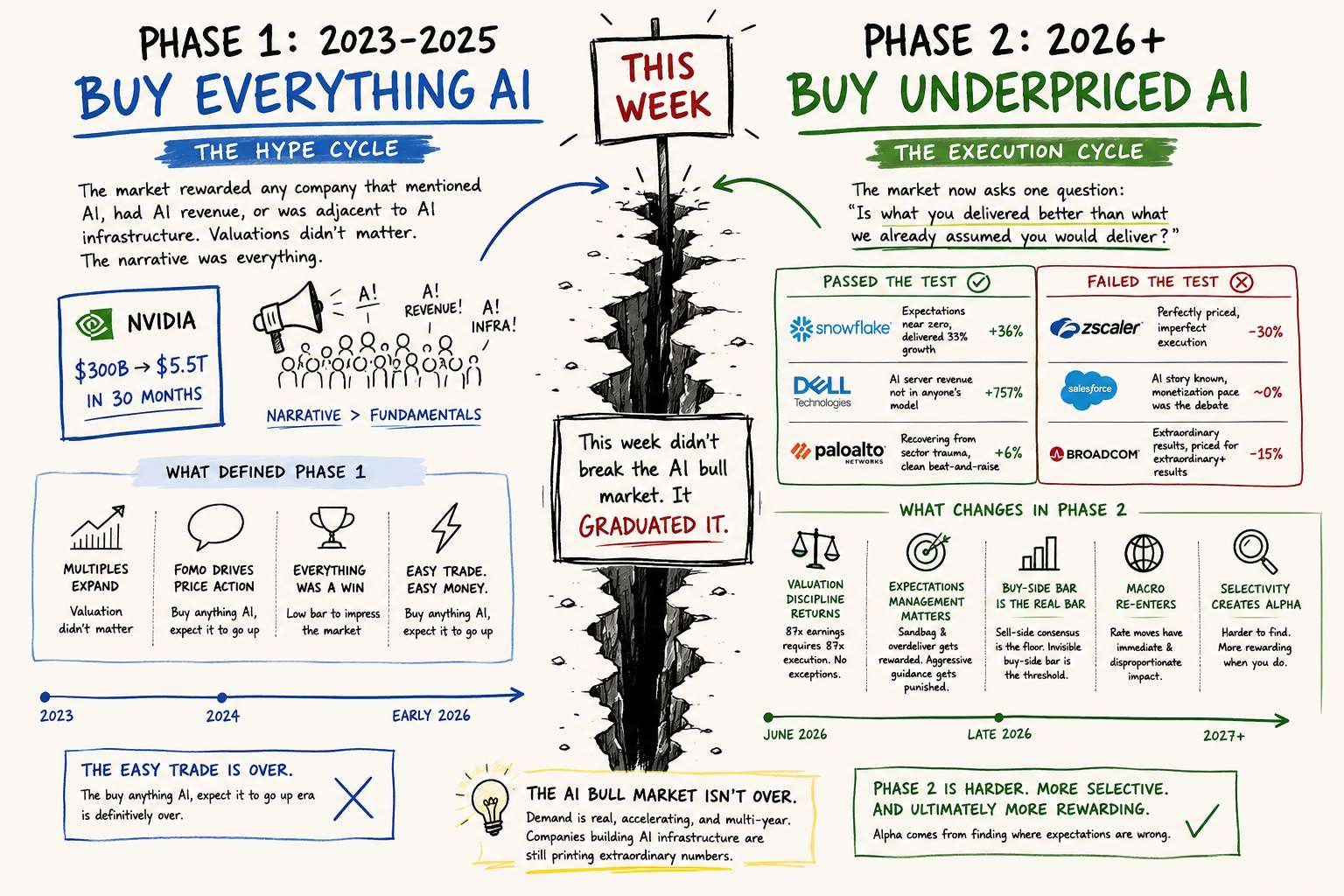

This week didn't break the AI bull market. It graduated it.

Phase 1 (2023–early 2026): The AI hype cycle. The market rewarded any company that mentioned AI, had AI revenue, or was adjacent to AI infrastructure. Valuations didn't matter. The narrative was everything. Nvidia going from $300B to $5.5T in 30 months is the defining data point of Phase 1.

Phase 2 (June 2026 onward): The execution cycle. Phase 1 ended not with a crash, but with a repricing. The market spent this week systematically repricing every major AI name based on one question: "Is what you delivered better than what we already assumed you would deliver?"

The companies that passed Phase 2's test: Snowflake (expectations near zero, delivered 33% growth), Dell (AI server revenue literally not in anyone's model at 757%), PANW (recovering from sector trauma, clean beat-and-raise).

The companies that failed Phase 2's test: Zscaler (perfectly priced, imperfect execution), Salesforce (AI story known, monetization pace was the debate), Broadcom (extraordinary results, but priced for extraordinary+ results).

What changes in Phase 2:

Valuation discipline returns. 87x earnings requires 87x execution. No exceptions.

Expectations management becomes a competitive advantage. The companies that sandbag guidance and overdeliver will be rewarded. The ones that set aggressive guidance will be punished on any shortfall.

The buy-side bar replaces earnings beats as the primary signal. Sell-side consensus is the floor. The invisible buy-side bar is the real threshold.

Macro re-enters the equation. In Phase 1, rate uncertainty was an inconvenience. In Phase 2, with multiples still extended, rate moves have immediate and disproportionate impact on stock prices.

The AI bull market isn't over. The companies building AI infrastructure are still printing extraordinary numbers. The demand is real, accelerating, and multi-year. But the easy trade — buy anything AI, expect it to go up — is definitively over.

Phase 2 is harder, more selective, and ultimately more rewarding for investors who do the work to find where expectations are wrong.

Welcome to the real AI trade.

Phase 1 (2023–early 2026): The AI hype cycle. The market rewarded any company that mentioned AI, had AI revenue, or was adjacent to AI infrastructure. Valuations didn't matter. The narrative was everything. Nvidia going from $300B to $5.5T in 30 months is the defining data point of Phase 1.

Phase 2 (June 2026 onward): The execution cycle. Phase 1 ended not with a crash, but with a repricing. The market spent this week systematically repricing every major AI name based on one question: "Is what you delivered better than what we already assumed you would deliver?"

The companies that passed Phase 2's test: Snowflake (expectations near zero, delivered 33% growth), Dell (AI server revenue literally not in anyone's model at 757%), PANW (recovering from sector trauma, clean beat-and-raise).

The companies that failed Phase 2's test: Zscaler (perfectly priced, imperfect execution), Salesforce (AI story known, monetization pace was the debate), Broadcom (extraordinary results, but priced for extraordinary+ results).

What changes in Phase 2:

Valuation discipline returns. 87x earnings requires 87x execution. No exceptions.

Expectations management becomes a competitive advantage. The companies that sandbag guidance and overdeliver will be rewarded. The ones that set aggressive guidance will be punished on any shortfall.

The buy-side bar replaces earnings beats as the primary signal. Sell-side consensus is the floor. The invisible buy-side bar is the real threshold.

Macro re-enters the equation. In Phase 1, rate uncertainty was an inconvenience. In Phase 2, with multiples still extended, rate moves have immediate and disproportionate impact on stock prices.

The AI bull market isn't over. The companies building AI infrastructure are still printing extraordinary numbers. The demand is real, accelerating, and multi-year. But the easy trade — buy anything AI, expect it to go up — is definitively over.

Phase 2 is harder, more selective, and ultimately more rewarding for investors who do the work to find where expectations are wrong.

Welcome to the real AI trade.

95

30

9

Sensitive-Fix8857:Feels like Phase 2 starts now. I’m watching SNOW and DELL for execution clarity before adding to my AI sleeve.

Wheremytendies:The math checks out: SNOW at 33% growth while expectations were near zero, DELL with 757% AI server revenue, PANW recovering. If multiples are disciplined, 87x requires consistency. I’m favoring SNOW and DELL over ZS and CRM until execution proves itself.

See all comments

View post details

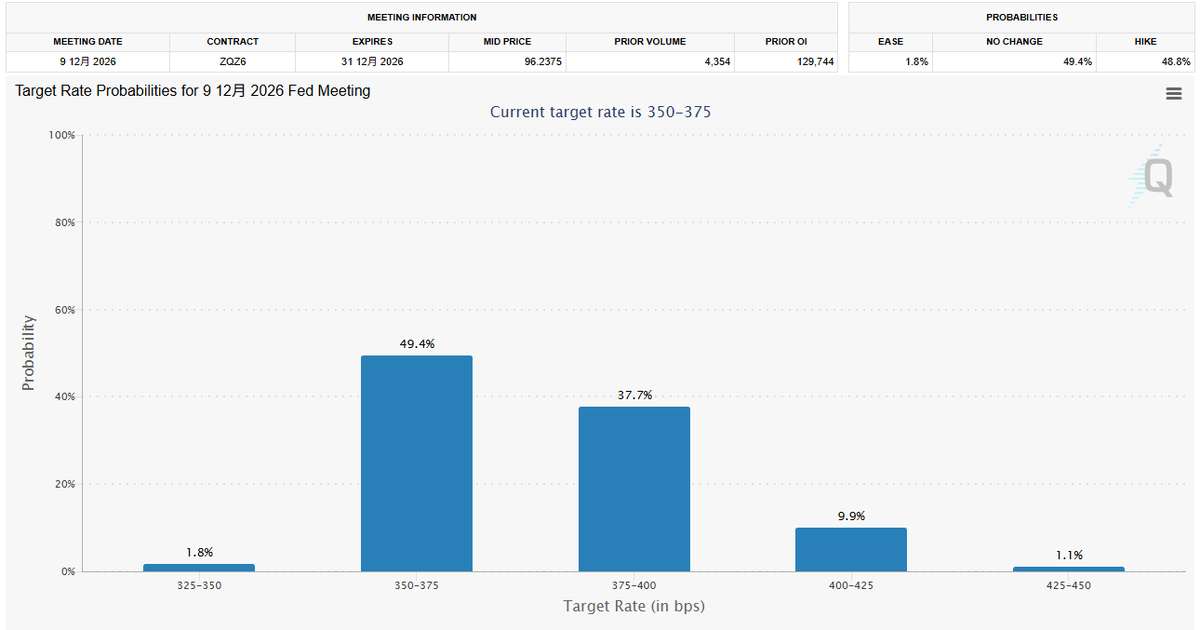

Federal Reserve Warsh June 2026 press conference 或 Fed interest rate decision June 2026

Today's NFP isn't just a jobs number. It's the opening argument in a trial that concludes on June 17.

Here's the full context of what Warsh inherits at his first major press conference as Fed Chair:

Inflation: PCE at 3.8% YoY in April, above the 2% target. PPI running at 6.0%. Not cooling fast enough.

Labor market: April +115K, beating 64K consensus by nearly 2x. ADP May at 122K. The market is resilient despite the Iran conflict, oil volatility, and rate uncertainty.

Oil: WTI oscillating between $88–93 depending on Iran headlines. Goldman's adverse scenario still has Brent at $115 if Hormuz reopens slowly.

AI capex: Broadcom guided $16B in AI chips next quarter. Dell has $24.4B in AI orders. The private sector is spending aggressively on AI infrastructure regardless of rates.

The Fed's dilemma: the traditional "soft jobs = rate cut" logic doesn't apply cleanly when inflation is still running hot and AI-driven capex is keeping the economy above stall speed. Warsh has to navigate a press conference where every answer risks either spooking the bond market or emboldening the equity market.

Today's NFP sets the tone. If it comes in soft, Warsh can be mildly dovish. If it's hot, he has to be hawkish — and the market re-prices June 17 from a "hold" to a potential "hawkish hold with rate hike optionality."

That distinction is worth 200–300 points on the S&P 500.

Today's NFP isn't just a jobs number. It's the opening argument in a trial that concludes on June 17.

Here's the full context of what Warsh inherits at his first major press conference as Fed Chair:

Inflation: PCE at 3.8% YoY in April, above the 2% target. PPI running at 6.0%. Not cooling fast enough.

Labor market: April +115K, beating 64K consensus by nearly 2x. ADP May at 122K. The market is resilient despite the Iran conflict, oil volatility, and rate uncertainty.

Oil: WTI oscillating between $88–93 depending on Iran headlines. Goldman's adverse scenario still has Brent at $115 if Hormuz reopens slowly.

AI capex: Broadcom guided $16B in AI chips next quarter. Dell has $24.4B in AI orders. The private sector is spending aggressively on AI infrastructure regardless of rates.

The Fed's dilemma: the traditional "soft jobs = rate cut" logic doesn't apply cleanly when inflation is still running hot and AI-driven capex is keeping the economy above stall speed. Warsh has to navigate a press conference where every answer risks either spooking the bond market or emboldening the equity market.

Today's NFP sets the tone. If it comes in soft, Warsh can be mildly dovish. If it's hot, he has to be hawkish — and the market re-prices June 17 from a "hold" to a potential "hawkish hold with rate hike optionality."

That distinction is worth 200–300 points on the S&P 500.

182

49

12

Ok_Manufacturer2112:Seen this movie: sticky inflation, resilient labor, then a pause. I'd expect choppy moves, not clear direction, until wage growth cools.

ChxmpV2:Why does every Fed talk move SPY 200 points?

See all comments

View post details

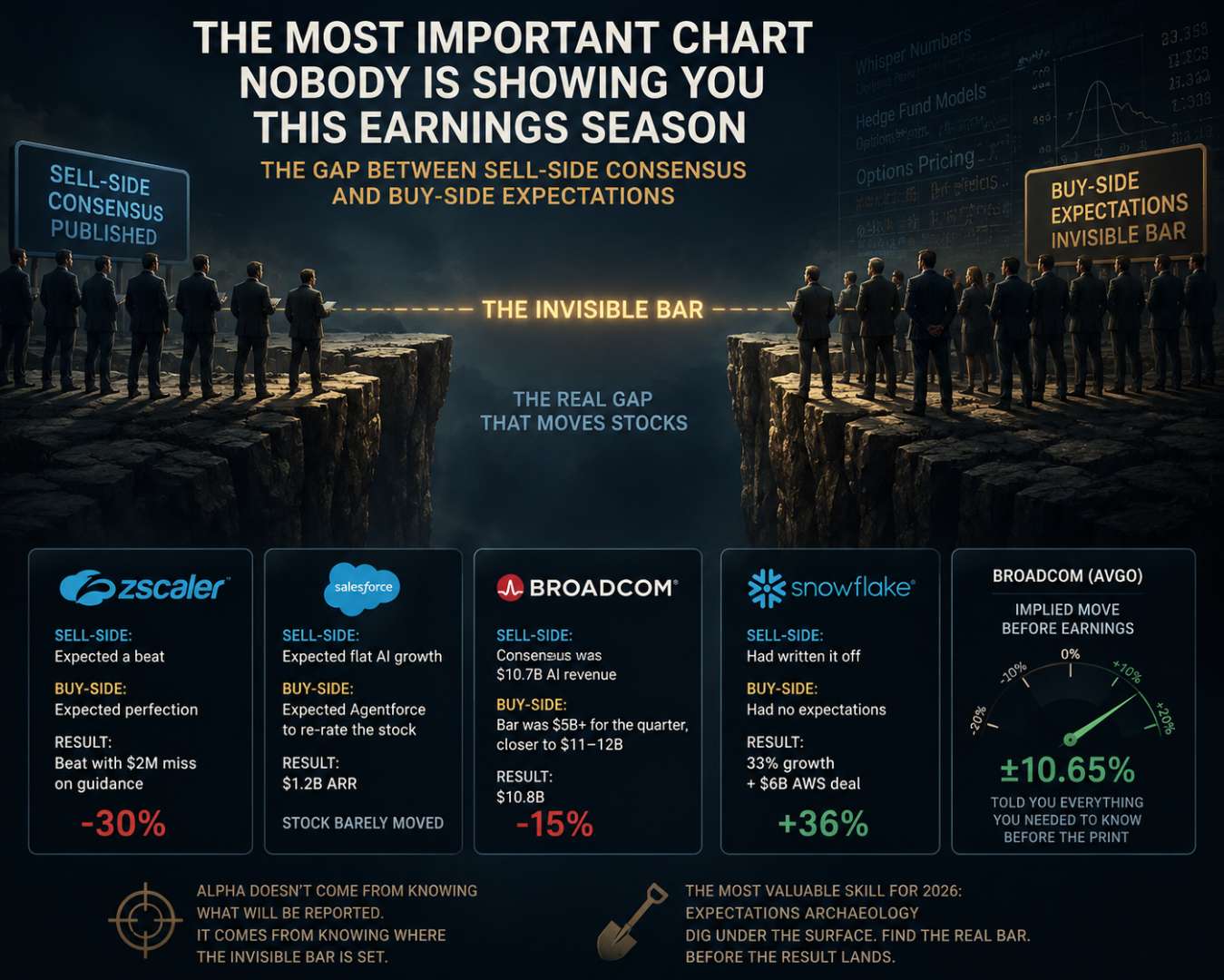

The most important chart nobody is showing you this earnings season isn't a stock chart. It's an invisible one — the gap between sell-side consensus and buy-side expectations.

Here's how it worked this cycle:

$ZS : Sell-side expected a beat. Buy-side expected perfection. Got a beat with a $2M miss on guidance. −30%.

$CRM : Sell-side expected flat AI growth. Buy-side expected Agentforce to re-rate the stock. Got $1.2B ARR. Stock barely moved.

$AVGO : Sell-side consensus was $10.7B AI revenue. Buy-side bar was $5B+ for the quarter, closer to $11–12B. Got $10.8B. −15%.

$SNOW : Sell-side had written it off. Buy-side had no expectations. Got 33% growth + $6B AWS deal. +36%.

The pattern is now undeniable: alpha in this market doesn't come from knowing what AI companies will report. It comes from knowing where the invisible bar is set — and whether the result clears it. That bar isn't published anywhere. It lives in hedge fund models, whisper numbers, and options pricing. The ±10.65% implied move on AVGO told you everything you needed to know before the print.

For the rest of 2026, the most valuable skill isn't fundamental analysis. It's expectations archaeology — digging under the surface to find where the real bar is buried, before the result lands.

Here's how it worked this cycle:

$ZS : Sell-side expected a beat. Buy-side expected perfection. Got a beat with a $2M miss on guidance. −30%.

$CRM : Sell-side expected flat AI growth. Buy-side expected Agentforce to re-rate the stock. Got $1.2B ARR. Stock barely moved.

$AVGO : Sell-side consensus was $10.7B AI revenue. Buy-side bar was $5B+ for the quarter, closer to $11–12B. Got $10.8B. −15%.

$SNOW : Sell-side had written it off. Buy-side had no expectations. Got 33% growth + $6B AWS deal. +36%.

The pattern is now undeniable: alpha in this market doesn't come from knowing what AI companies will report. It comes from knowing where the invisible bar is set — and whether the result clears it. That bar isn't published anywhere. It lives in hedge fund models, whisper numbers, and options pricing. The ±10.65% implied move on AVGO told you everything you needed to know before the print.

For the rest of 2026, the most valuable skill isn't fundamental analysis. It's expectations archaeology — digging under the surface to find where the real bar is buried, before the result lands.

78

23

4

makybo91:Rates stay higher, whispers matter more than headlines.

Mojojojo3030:So basically, analysts say X, hedge funds expect Y, and if Y is missed, it drops. Feels like noise; how do we actually verify those whispers?

See all comments

View post details

Most people read Trump's AI executive order as a headline. Here's the actual mechanism and who wins.

The order does three concrete things: it asks AI companies to voluntarily submit frontier models for government review 30 days before release; it directs agencies to build an "AI cybersecurity clearinghouse"; and it accelerates federal procurement of AI systems. Beneath those three lines is a $30 billion Pentagon AI budget that is now actively looking for deployment vehicles.

The direct beneficiary map: Palantir (PLTR) is already embedded — its Maven AI system compressed Iran targeting cycles from days to minutes and is operationally live. CrowdStrike (CRWD) and Palo Alto (PANW) benefit from the cybersecurity hardening mandate. Microsoft (MSFT) and Oracle (ORCL) are the cloud infrastructure layer for most federal AI deployments. Booz Allen Hamilton (BAH) is the systems integrator that translates policy into contracts.

The less obvious beneficiary: Anthropic. The order was partly triggered by security concerns over models like Claude that can exploit vulnerabilities at unprecedented speeds — the Pentagon is simultaneously designating it a "supply-chain risk" and remaining its largest government AI user. That tension doesn't resolve cleanly, but it guarantees Anthropic stays central to federal AI policy for years.

This isn't a one-day trade. It's a multi-year government procurement cycle that most equity models haven't fully priced.

The order does three concrete things: it asks AI companies to voluntarily submit frontier models for government review 30 days before release; it directs agencies to build an "AI cybersecurity clearinghouse"; and it accelerates federal procurement of AI systems. Beneath those three lines is a $30 billion Pentagon AI budget that is now actively looking for deployment vehicles.

The direct beneficiary map: Palantir (PLTR) is already embedded — its Maven AI system compressed Iran targeting cycles from days to minutes and is operationally live. CrowdStrike (CRWD) and Palo Alto (PANW) benefit from the cybersecurity hardening mandate. Microsoft (MSFT) and Oracle (ORCL) are the cloud infrastructure layer for most federal AI deployments. Booz Allen Hamilton (BAH) is the systems integrator that translates policy into contracts.

The less obvious beneficiary: Anthropic. The order was partly triggered by security concerns over models like Claude that can exploit vulnerabilities at unprecedented speeds — the Pentagon is simultaneously designating it a "supply-chain risk" and remaining its largest government AI user. That tension doesn't resolve cleanly, but it guarantees Anthropic stays central to federal AI policy for years.

This isn't a one-day trade. It's a multi-year government procurement cycle that most equity models haven't fully priced.

99

28

12

Sea-Ingenuity-9508:Trend looks intact: PLTR and CRWD are already up on this, and PANW/MSFT keep stacking federal contracts. If the clearinghouse ramps, we’ll see more buybacks and guidance hikes, which momentum traders should chase.

Summerdaysengineer:Procurement cycles plus higher rates usually mean slower deployments.

See all comments

View post details

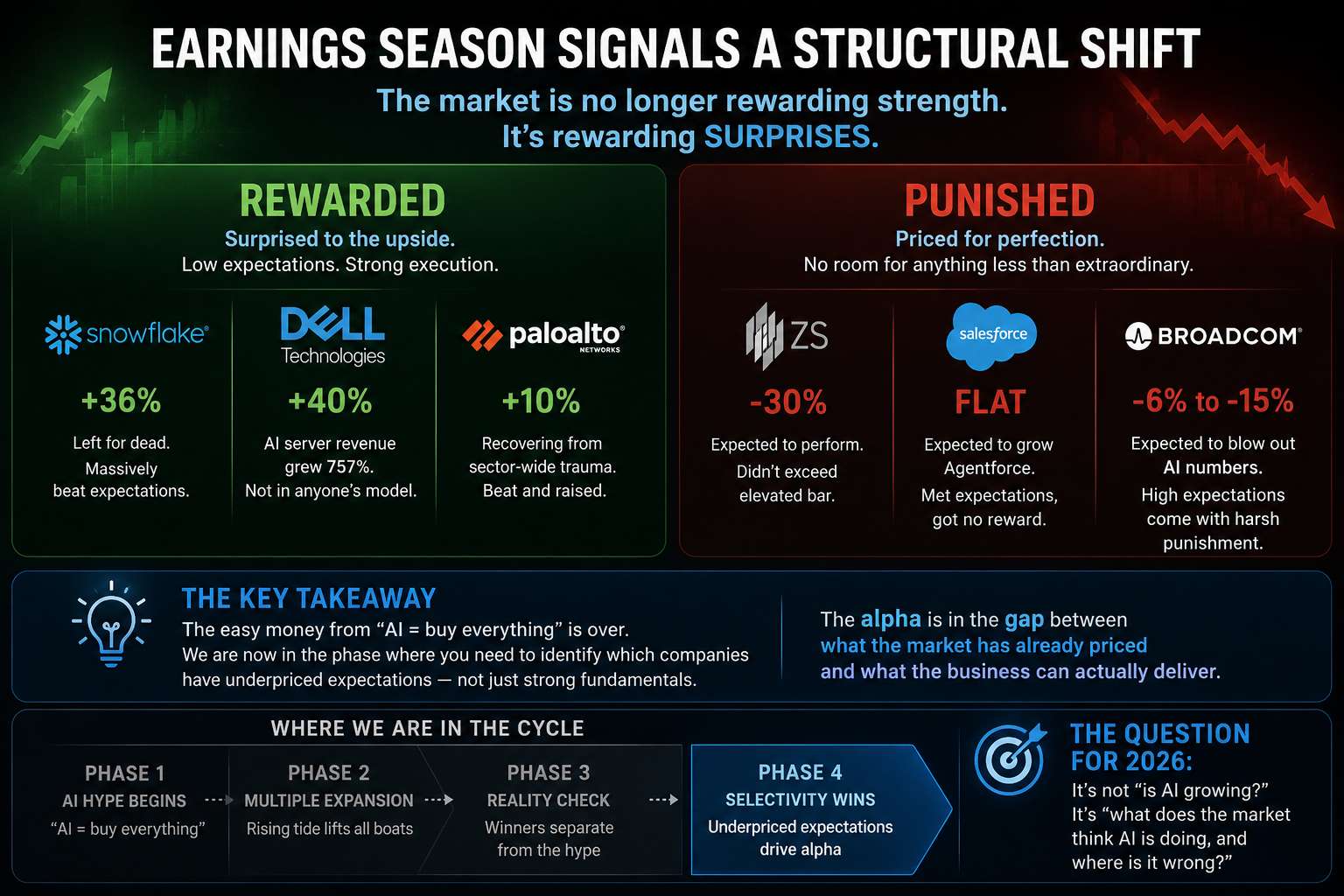

Step back from AVGO for a moment and look at the full picture of this earnings season. Something structural has changed, and it matters for how you position the next six months.

The companies that got rewarded this cycle — Snowflake (+36%), Dell (+40%), PANW (+10%) — all shared one characteristic: they delivered results that were genuinely surprising relative to lowered expectations. SNOW had been left for dead. DELL's AI server revenue growing 757% was not in anyone's model. PANW was recovering from sector-wide trauma.

The companies that got punished — ZS (−30%), CRM (flat), AVGO (−6–15%) — were priced for perfection going in. ZS was expected to perform. CRM was expected to grow Agentforce. AVGO was expected to blow out AI numbers. There was no room for anything less than extraordinary.

This tells you something important about where we are in the cycle: the easy money from "AI = buy everything" is over. We are now in the phase where you need to identify which companies have underpriced expectations — not just strong fundamentals. The alpha is in the gap between what the market has already priced and what the business can actually deliver.

For the rest of 2026, the most important question isn't "is AI growing?" It's "what does the market think AI is doing, and where is it wrong?"

The companies that got rewarded this cycle — Snowflake (+36%), Dell (+40%), PANW (+10%) — all shared one characteristic: they delivered results that were genuinely surprising relative to lowered expectations. SNOW had been left for dead. DELL's AI server revenue growing 757% was not in anyone's model. PANW was recovering from sector-wide trauma.

The companies that got punished — ZS (−30%), CRM (flat), AVGO (−6–15%) — were priced for perfection going in. ZS was expected to perform. CRM was expected to grow Agentforce. AVGO was expected to blow out AI numbers. There was no room for anything less than extraordinary.

This tells you something important about where we are in the cycle: the easy money from "AI = buy everything" is over. We are now in the phase where you need to identify which companies have underpriced expectations — not just strong fundamentals. The alpha is in the gap between what the market has already priced and what the business can actually deliver.

For the rest of 2026, the most important question isn't "is AI growing?" It's "what does the market think AI is doing, and where is it wrong?"

126

33

8

kawa_yt332:SNOW +36%, DELL +40% on surprise, but CRM flat and ZS -30%. If AI growth is real, why such divergence? Feels like pricing power, not demand.

chatofwallst:Everyone’s cheering SNOW and DELL, but I’m skeptical this trend sticks. Data center capex is slowing, enterprise budgets are tight, and AI workloads may not scale as promised. PANW’s recovery feels fragile without broader demand.

See all comments

View post detailsAVGO

Ok here me out. Earnings were so strong but they were looking for a massive raise due to raised AI demand but they had reported AI demand remains explosive, AI revenue beat own forecast, Q3 revenue expected to reach $16BN, over 200%+ YoY growth.

Broadcom is also up 70%+ in the last 2 months so lets be fair... it was a bit overbought for such a giant. I believe this dip right to the 34MA will shape up for the next leg up through summer & fall for 550.

My thesis hasn't change. It's a matter of building a base in the same range where it was just lastweek

Ok here me out. Earnings were so strong but they were looking for a massive raise due to raised AI demand but they had reported AI demand remains explosive, AI revenue beat own forecast, Q3 revenue expected to reach $16BN, over 200%+ YoY growth.

Broadcom is also up 70%+ in the last 2 months so lets be fair... it was a bit overbought for such a giant. I believe this dip right to the 34MA will shape up for the next leg up through summer & fall for 550.

My thesis hasn't change. It's a matter of building a base in the same range where it was just lastweek

145

41

9

flylowe:Buy the dip to 34MA, or wait for Broadcom?

Complete-Meaning2977:Everyone’s cheering the beat, but the stock was already frothy; feels like classic AI hype chasing itself.

See all comments

View post details

IBM stock up 8% last week because Trump said it had a "nice price" years ago.

AVGO up 33% YTD because its AI chips power half the internet.

Both are up. Only one makes sense.

AVGO up 33% YTD because its AI chips power half the internet.

Both are up. Only one makes sense.

68

21

6

pipjoh:One stock riding political hype, another on AI moats.

curiouscuriel:Feels weird that a political quote can swing a stock this much. I’m cautiously optimistic but still uneasy about the noise.

See all comments

View post details

Everyone's focused on AVGO tonight.

Nobody's talking about the fact that ADP jobs + ISM Services both print today — two days before NFP — two weeks before the Fed meeting.

The AI trade doesn't exist in a vacuum. Rates are still gravity.

Nobody's talking about the fact that ADP jobs + ISM Services both print today — two days before NFP — two weeks before the Fed meeting.

The AI trade doesn't exist in a vacuum. Rates are still gravity.

101

28

5

Xtianus21:Feels like another AI hype pop; I’m not buying it.

ItsCrypticYT:Watching AVGO on a fade if ADP disappoints.

See all comments

View post details

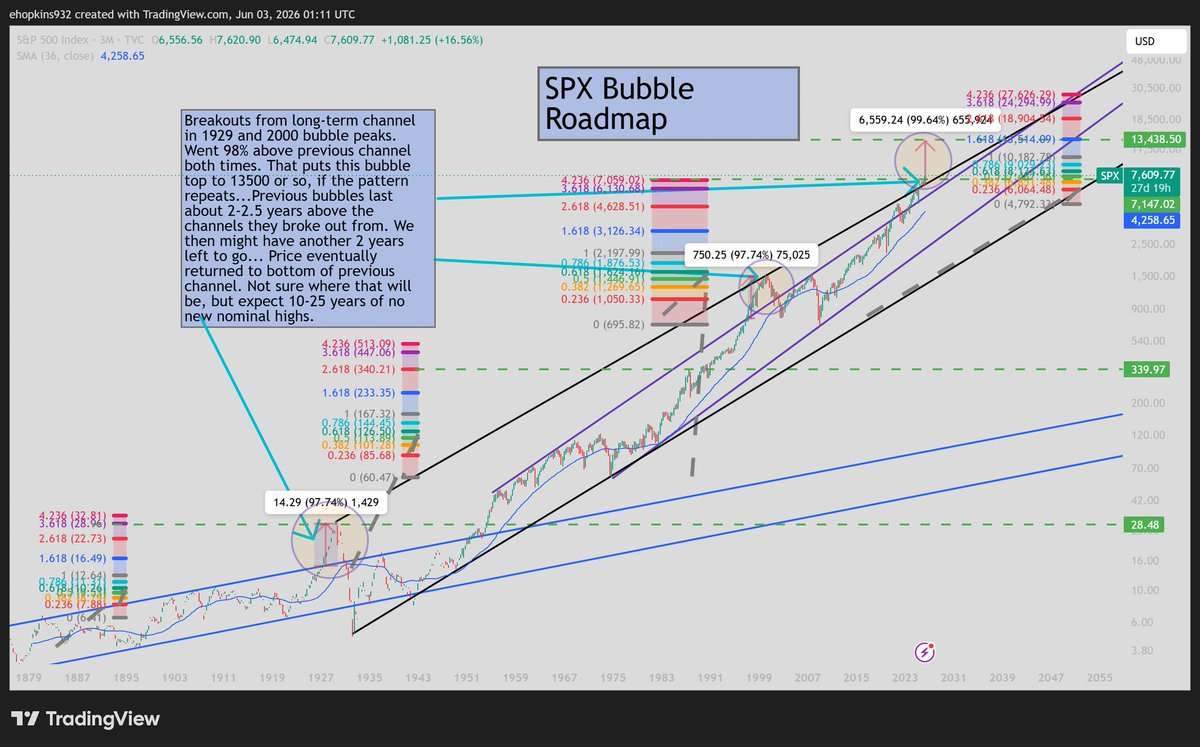

SPX Bubble Roadmap

See the caption in the chart. SPX has broken out and back tested the resistance line from the 1929 and 2000 bubble tops. Based on past moves, we should expect to see about a 98% gained from the breakout over 2 to 2.5 years (to about 13,500) followed by no new nominal highs for 15 to 25 years.

Any move confirmed below the upper black support line, prior to a blow off top, negate this thesis.

$spx

$spy

See the caption in the chart. SPX has broken out and back tested the resistance line from the 1929 and 2000 bubble tops. Based on past moves, we should expect to see about a 98% gained from the breakout over 2 to 2.5 years (to about 13,500) followed by no new nominal highs for 15 to 25 years.

Any move confirmed below the upper black support line, prior to a blow off top, negate this thesis.

$spx

$spy

35

9

2

Blackhole1123:Feels like another hype trap again.

Megadragon1604:How much of this thesis hinges on rates staying low? If the Fed pivots, does the breakout unwind fast, or does liquidity cushion it?

See all comments

View post details

Step back from the noise for a second.

In the past 10 days:

— Micron crossed $1 trillion

— Dell's AI orders hit $24.4B in one quarter

— Snowflake grew 33% and signed a $6B AWS deal

— PANW's security ARR crossed $8B

The AI buildout isn't slowing. If anything, it's accelerating.

In the past 10 days:

— Micron crossed $1 trillion

— Dell's AI orders hit $24.4B in one quarter

— Snowflake grew 33% and signed a $6B AWS deal

— PANW's security ARR crossed $8B

The AI buildout isn't slowing. If anything, it's accelerating.

139

41

12

TheBetterTheta:Hard to ignore the numbers: $1T crossing for MU, $24.4B in Dell AI orders, SNOW +33% and a $6B AWS deal, PANW ARR over $8B. That’s multi-year spend ramping. I’m leaning overweight AI hardware and data platforms.

daynightcase:Tape looks like classic AI momentum: SNOW ripping on AWS, PANW climbing on security spend, and MU riding the memory cycle. If volume stays heavy, this could keep running until guidance or earnings cool the narrative.

See all comments

View post details

$NVDA $MU $AMD $SPY Hyperscalers are increasing their equity to fund AI expansion Google just announced 80B and META is following suit with Microsoft and Amazon likely to join soon I see this as a sign that Nvidia might boost its money soon so I bought 215C end of July calls for V play Roughly 12% below its all-time high is a decent dip for the AI leader calls offer better returns in my opinion Have a great weekend Puts were awesome today 😂👊

Like

Comment

Share

View post details

$SOXX closed at $539.77 — between -1σ $545.78 and -2σ $538.29. Down $62.95 from Wednesday's close of $602.72 over three sessions. AVGO -16%. KOSPI -6%. The AI concentration trade is still winding down. With VIX at 21.51, the bands have stretched — -2σ $538.29 is the floor Monday, -3σ $530.79 is the trapdoor. EMA8 rollover on the Dirty Dozen confirms what SOXX is showing. Full breakdown on Substack. #SOXX #semiconductors #trading https://kingcambo812.substack.com/p/evening-debrief-june-5-2026-kill-switch-detonated-dog-didnt-bark?utm_source=activity_item

117

30

6

RiverBink:Semis still look fragile: AVGO’s -16% and MU’s pullback suggest demand softening beyond AI hype. If hyperscalers cap spending or cloud budgets tighten, these names lag while broader tech rallies.

KlutzyCasual:Watching SOXX near -2σ at 538.29; I’m fading bounces into 545–548 with tight stops under 535. If it reclaims 550, I’ll short into strength. Meanwhile, AVGO and MU pops look like distribution.

See all comments

View post details

$ORCL Markets took a hit today. Wondering where all that new cash will go. ORCL has been overlooked in AI for too long. I'm confident it changes soon. Stay bullish. Our time is coming!

130

30

14

Historical_Hearing76:Feels like $ORCL is just getting warmed up after the dip. The cash infusion could mean buybacks, dividends, or AI acquisitions. Watching for a pullback to retest the recent lows before considering a starter.

pls-send-bobs-vagene:For a balanced book, how much weight do you add to $ORCL versus MSFT/NVDA after the cash announcement?

See all comments

40

10

2

ipsidicit:Everyone assumes FIFA = safe harbor, but that's the trap. Liquidity evaporates on weak volume, spreads widen, and options pricing collapses. If you're writing calls into a pop, you're basically betting the pop doesn't stick.

See all comments

View post details

$CRWD Stock dropping? Price to Sales is 35.7, Trailing PE 401, Forward PE 149, Revenue Growth FY27 22-23%. Compare to Sentinel One (S) and see the gap

73

20

11

View post details

$SOXL I made over 11 times on SOXL 7-figure position, life changing money, bless no matter what happens, but I believe AI will keep going!

Like

Comment

Share

View post details

$SOXL Trump might say something about AI and tech that could push this up. For now, it could be near the top but expect a bounce Monday

93

25

12

79

18

6

View post details

$INTC A strong job market means more people can afford laptops, computers, and phones with AI features which should help semiconductor companies. Selling off today is overreacting and will bounce back soon. That's why Trump is reaching out to AI leaders to boost government investment in AI firms next week.

Like

Comment

Share

No More Posts

Disclaimer: The above is a summary showing certain market information. AInvest is not responsible for any data errors, omissions or other information that may be displayed incorrectly as the data is derived from various resources. Communications displaying market prices, data and other information available in this post are meant for purely informational purposes and are not intended as an offer or solicitation for the purchase or sale of any security. Please do your own research or consult a professional before making investment decisions. Keep in mind that past performance of any security or financial product does not guarantee future returns.Report an Issue

CONTACT US

Email: support@ainvest.com

Address: 330 7th Ave, Suite 902, New York, NY 10001, US

Copyright 2026 AInvest Fintech Inc. All rights reserved.