June 8 Daily Discussion: The AI Hardware Trade Just Broke. Can Apple's Software Story Save It?

19.1KViews

0Posts

What’s next for AI?

612

Votes

Closes in 1d 12h

View post details

Most of the WWDC previews are focused on Siri features. That's missing the bigger picture.

Apple's real AI moat isn't Siri. It's the combination of three things no other AI company has simultaneously: on-device compute, trusted hardware, and a closed ecosystem.

On-device compute: Apple Silicon's Neural Engine processes AI tasks locally without sending data to the cloud. This isn't just a privacy feature — it's a structural cost advantage. Every AI query that runs on-device costs Apple nothing in compute. Google, Microsoft, and OpenAI pay for every inference. At 2.2 billion devices, even a fraction of queries running locally represents a cost structure that cloud-first AI companies simply cannot replicate.

Trusted hardware: Apple is the only company with a consumer hardware brand trusted enough that users willingly store their most sensitive data — health, payments, messages, location, photos — entirely within its ecosystem. That data is the fuel for personalized AI. Siri 2.0 with access to your health records, your calendar, your emails, and your location history is categorically more useful than a cloud AI that knows nothing about you.

The closed ecosystem: App Store, iCloud, Apple Pay, Apple TV+, Apple Fitness. Every AI enhancement in iOS 27 makes every other Apple service stickier. The upgrade supercycle thesis isn't about Siri being impressive in a demo. It's about Siri being the connective tissue that makes all $100B of Apple's services revenue compound faster.

Morgan Stanley is right that WWDC could be an "AI winner" inflection point. But not because the features will be groundbreaking in isolation. Because Apple's distribution advantage — 2.2 billion trusted devices — means even a modest AI execution creates a flywheel that no one else can replicate at scale.

Apple's real AI moat isn't Siri. It's the combination of three things no other AI company has simultaneously: on-device compute, trusted hardware, and a closed ecosystem.

On-device compute: Apple Silicon's Neural Engine processes AI tasks locally without sending data to the cloud. This isn't just a privacy feature — it's a structural cost advantage. Every AI query that runs on-device costs Apple nothing in compute. Google, Microsoft, and OpenAI pay for every inference. At 2.2 billion devices, even a fraction of queries running locally represents a cost structure that cloud-first AI companies simply cannot replicate.

Trusted hardware: Apple is the only company with a consumer hardware brand trusted enough that users willingly store their most sensitive data — health, payments, messages, location, photos — entirely within its ecosystem. That data is the fuel for personalized AI. Siri 2.0 with access to your health records, your calendar, your emails, and your location history is categorically more useful than a cloud AI that knows nothing about you.

The closed ecosystem: App Store, iCloud, Apple Pay, Apple TV+, Apple Fitness. Every AI enhancement in iOS 27 makes every other Apple service stickier. The upgrade supercycle thesis isn't about Siri being impressive in a demo. It's about Siri being the connective tissue that makes all $100B of Apple's services revenue compound faster.

Morgan Stanley is right that WWDC could be an "AI winner" inflection point. But not because the features will be groundbreaking in isolation. Because Apple's distribution advantage — 2.2 billion trusted devices — means even a modest AI execution creates a flywheel that no one else can replicate at scale.

49

12

2

Option_Closeout:Is AAPL already riding the AI momentum wave?

Silver-Feeling6281:Does this shift reduce cloud spend and pressure MSFT/GOOGL?

See all comments

View post details

The selloff last week revealed something important about how the market prices different types of AI exposure — and why the rotation from hardware to software could be both inevitable and violent.

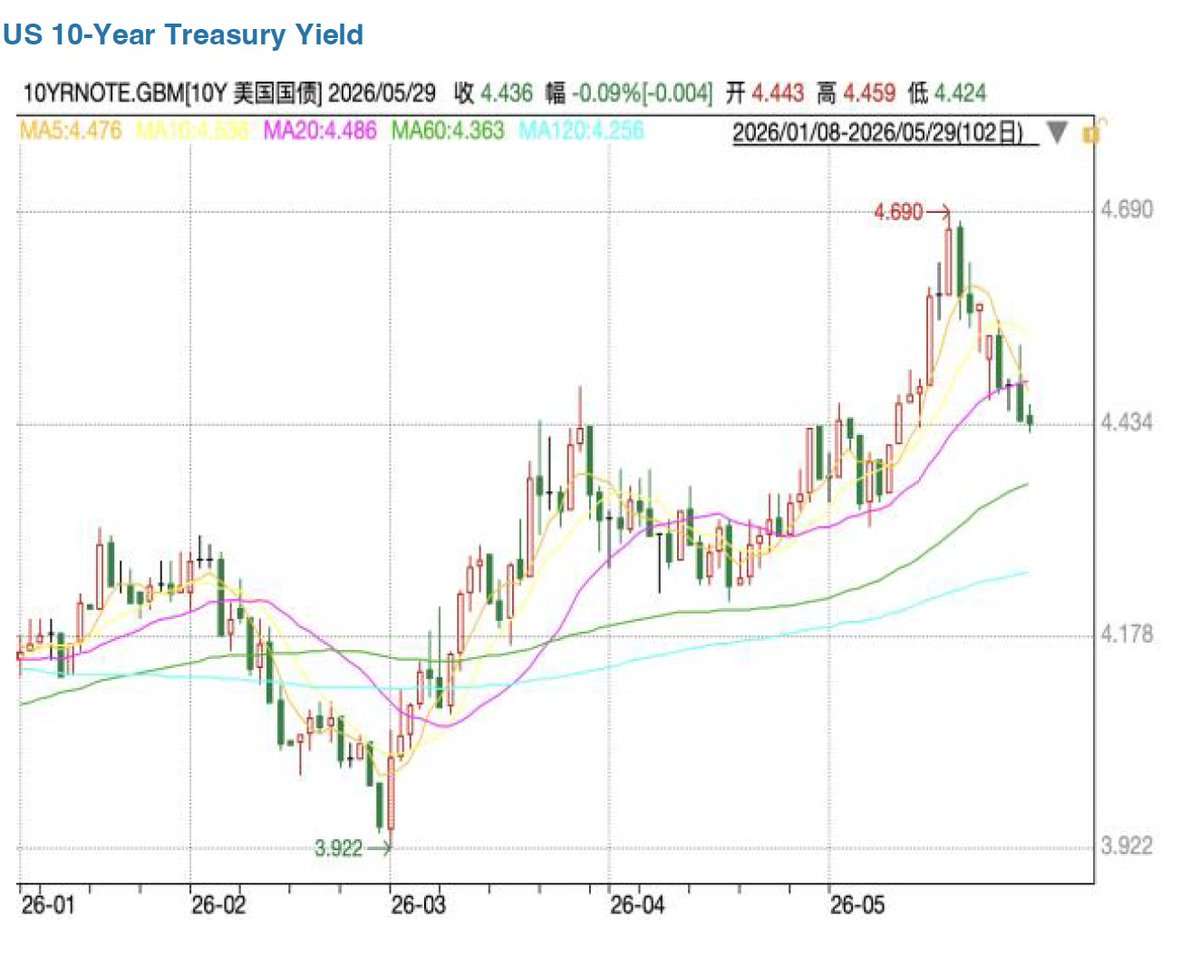

Hardware AI (Nvidia, Broadcom, AMD, Micron) is a capex cycle bet. You're essentially betting that hyperscalers continue spending $50–60B per quarter on AI infrastructure indefinitely. The thesis is simple and powerful when rates are low: borrow cheap, build fast, the ROI comes later. When rates spike — as they did Friday with the 10Y hitting 4.54% — the "ROI comes later" part becomes a problem. Higher discount rates make future cash flows worth less. Hardware AI stocks get hit hardest because their earnings are largely front-loaded (the spending is happening now) while the monetization is still uncertain.

Software AI (Apple, Salesforce, ServiceNow, Microsoft) is a monetization cycle bet. You're betting that AI features drive incremental revenue — higher prices, lower churn, more seats, new services. The multiple is lower (40-60x vs 80-90x for hardware), but so is the sensitivity to rates. More importantly, software AI doesn't require the customer to keep spending on infrastructure. Once the AI feature is in the product, the revenue recurs.

The irony: the market spent six months rotating INTO hardware AI because the ROI story was clearer. Now, with rates rising and hardware stocks repricing, the rotation is reversing. Software AI — which looked boring compared to Nvidia's vertical chart — suddenly looks like the safer bet.

Apple sits at the intersection. 2.2 billion devices is the distribution advantage no hyperscaler can match. If Siri 2.0 drives even a 5% increase in services revenue, that's $5B+ in high-margin, recurring revenue that doesn't require a data center to scale.

Today's WWDC is the first real test of whether the rotation from hardware AI to software AI is real — or just a wishful narrative.

Hardware AI (Nvidia, Broadcom, AMD, Micron) is a capex cycle bet. You're essentially betting that hyperscalers continue spending $50–60B per quarter on AI infrastructure indefinitely. The thesis is simple and powerful when rates are low: borrow cheap, build fast, the ROI comes later. When rates spike — as they did Friday with the 10Y hitting 4.54% — the "ROI comes later" part becomes a problem. Higher discount rates make future cash flows worth less. Hardware AI stocks get hit hardest because their earnings are largely front-loaded (the spending is happening now) while the monetization is still uncertain.

Software AI (Apple, Salesforce, ServiceNow, Microsoft) is a monetization cycle bet. You're betting that AI features drive incremental revenue — higher prices, lower churn, more seats, new services. The multiple is lower (40-60x vs 80-90x for hardware), but so is the sensitivity to rates. More importantly, software AI doesn't require the customer to keep spending on infrastructure. Once the AI feature is in the product, the revenue recurs.

The irony: the market spent six months rotating INTO hardware AI because the ROI story was clearer. Now, with rates rising and hardware stocks repricing, the rotation is reversing. Software AI — which looked boring compared to Nvidia's vertical chart — suddenly looks like the safer bet.

Apple sits at the intersection. 2.2 billion devices is the distribution advantage no hyperscaler can match. If Siri 2.0 drives even a 5% increase in services revenue, that's $5B+ in high-margin, recurring revenue that doesn't require a data center to scale.

Today's WWDC is the first real test of whether the rotation from hardware AI to software AI is real — or just a wishful narrative.

78

23

5

TeslaCoin1000000:I’m trimming speculative hardware and increasing software weight. Keeping cash for dips; if rates stay sticky, recurring AI revenue feels like the safer portfolio position.

therealchengarang:Volatility like this is where I nibble. If NVDA keeps selling out, I’ll add; if MSFT/AAPL show real AI stickiness, I’ll rotate.

See all comments

View post details

The 172K NFP print wasn't just a beat. It was a structural signal that the market had been pricing wrong for months.

Here's the context. Wall Street consensus was 85K — itself a downgrade from April's 115K. The prevailing narrative was: Iran conflict + oil shock + DOGE federal job cuts = labor market cooling. The Fed could afford to be patient. Rates would eventually come down.

172K shattered that narrative on three levels.

First, it confirmed the "war economy resilience" thesis. Despite a genuine geopolitical conflict that drove oil above $90, US private sector hiring accelerated. Healthcare added 40K+. Transportation and warehousing surged. The consumer economy is not breaking.

Second, it changes the Fed's calculus for June 17. Warsh now walks into his first press conference with a labor market running above trend, inflation still at 3.8% PCE and 6.0% PPI, and oil hovering near $93. A dovish statement becomes nearly impossible. The best-case scenario is a "neutral hold" — which the market will interpret as hawkish relative to prior expectations.

Third, and most importantly, it resets the discount rate for every high-multiple growth stock. At 4.54% on the 10-year, an 80x earnings AI stock needs to grow faster — or reprice lower. That math doesn't care about Broadcom's Q3 guide or Snowflake's AWS deal. It's pure arithmetic.

The NFP number didn't say AI is over. It said the free lunch is over. Growth has to justify valuation from here — not the other way around.

Here's the context. Wall Street consensus was 85K — itself a downgrade from April's 115K. The prevailing narrative was: Iran conflict + oil shock + DOGE federal job cuts = labor market cooling. The Fed could afford to be patient. Rates would eventually come down.

172K shattered that narrative on three levels.

First, it confirmed the "war economy resilience" thesis. Despite a genuine geopolitical conflict that drove oil above $90, US private sector hiring accelerated. Healthcare added 40K+. Transportation and warehousing surged. The consumer economy is not breaking.

Second, it changes the Fed's calculus for June 17. Warsh now walks into his first press conference with a labor market running above trend, inflation still at 3.8% PCE and 6.0% PPI, and oil hovering near $93. A dovish statement becomes nearly impossible. The best-case scenario is a "neutral hold" — which the market will interpret as hawkish relative to prior expectations.

Third, and most importantly, it resets the discount rate for every high-multiple growth stock. At 4.54% on the 10-year, an 80x earnings AI stock needs to grow faster — or reprice lower. That math doesn't care about Broadcom's Q3 guide or Snowflake's AWS deal. It's pure arithmetic.

The NFP number didn't say AI is over. It said the free lunch is over. Growth has to justify valuation from here — not the other way around.

45

12

1

thrwawyye:Holding MSFT and NVDA; not convinced this changes my thesis.

LeftHandedWave:Kinda nervous—did I miss the reset?

See all comments

View post details

Part 1: (What's the next move for Crypto and Stocks)

Friday, 5th June 2026, was one of the worst days for financial markets in the past 12 months. Nearly $2.5 trillion got wiped out in a single day. Stocks crashed hard, crypto and

$BTC

got hit, commodities dropped, $OIL weakened, $XAU sold off, and panic spread across almost every asset class. It is very rare to witness such a broad-based selloff where virtually everything gets sold together.

After digging much deeper into it, I came to understand that there were three major reasons behind this move.

1️⃣ The Mega IPO Liquidity Drain

The market has three massive upcoming IPOs on the horizon: $SpaceX, $OpenAI, and $Anthropic, carrying a combined valuation of around $4 trillion.

Now think about it for a moment. How will the funding for these offerings come from retail and institutional investors? Money doesn't magically appear. Large investors need liquidity, and liquidity is often raised by selling existing positions. Money never leaves the financial markets, it just rotates.

According to Business Insider reports, SpaceX and other IPO candidates will not be fast-tracked into the S&P 500 after all, but that doesn't change the fact that investors have been preparing for these listings. SpaceX alone is expected to raise approximately $75 billion, making it one of the largest IPO events in history.

When opportunities of this size emerge, money gets pulled from somewhere else. That "somewhere else" is often the market you're currently invested in.

2️⃣ Hot U.S. Jobs Data & Rate Hike Fears

The second major reason was the surprisingly strong U.S. employment data.

Reports suggested the U.S. economy added 172,000 jobs, while expectations were around 88,000, almost double the forecast.

This immediately changed the market's expectations. Strong employment data means the economy is still running hot, making it harder for the Federal Reserve to justify rate cuts. Instead, the possibility of further rate hikes gained momentum, with probabilities jumping from roughly 25% to 60%.

This pushed both the DXY (U.S. Dollar Index) and Treasury yields higher.

Historically, a strong DXY is one of the biggest headwinds for global financial markets. Even more importantly, whenever the U.S. 10-Year Treasury Yield remains above 4.5% while maintaining a bullish structure, financial markets tend to experience stress and liquidity pressure.

This is not a new narrative for me.

Since last year, I have repeatedly stated since last year that the market could eventually face a scenario where rates stay elevated and could hike for much longer than we expect. Persistent inflation, resilient economic data, rising energy prices, and geopolitical uncertainty have consistently supported that view.

Now, with a new Fed Chairman brought in by Trump, his key meeting scheduled within the next 10 days, elevated inflation concerns, double hot jobs data, high oil prices, and ongoing geopolitical tensions while the U.S. remains involved in global conflicts, investors simply do not know what comes next.

And when uncertainty rises, investors reduce risk.

Historically, Bitcoin and crypto are often among the first assets sold during risk-off events.

3️⃣ Cracks Starting to Appear in the AI Trade

The third major reason is that cracks are beginning to emerge in the AI trade.

Despite strong reports, Broadcom Inc. suffered a 15% decline, marking one of its worst performances of the year. The primary reason was simple: investors expected the company to raise its future revenue targets aggressively, and that didn't happen.

That single disappointment was enough to shake confidence across the entire AI space.

Broadcom's weakness quickly spread to other AI-related names, including NVIDIA, as investors started asking a very uncomfortable question:

"Are we paying too much simply because something has AI attached to its name?"

Friday, 5th June 2026, was one of the worst days for financial markets in the past 12 months. Nearly $2.5 trillion got wiped out in a single day. Stocks crashed hard, crypto and

$BTC

got hit, commodities dropped, $OIL weakened, $XAU sold off, and panic spread across almost every asset class. It is very rare to witness such a broad-based selloff where virtually everything gets sold together.

After digging much deeper into it, I came to understand that there were three major reasons behind this move.

1️⃣ The Mega IPO Liquidity Drain

The market has three massive upcoming IPOs on the horizon: $SpaceX, $OpenAI, and $Anthropic, carrying a combined valuation of around $4 trillion.

Now think about it for a moment. How will the funding for these offerings come from retail and institutional investors? Money doesn't magically appear. Large investors need liquidity, and liquidity is often raised by selling existing positions. Money never leaves the financial markets, it just rotates.

According to Business Insider reports, SpaceX and other IPO candidates will not be fast-tracked into the S&P 500 after all, but that doesn't change the fact that investors have been preparing for these listings. SpaceX alone is expected to raise approximately $75 billion, making it one of the largest IPO events in history.

When opportunities of this size emerge, money gets pulled from somewhere else. That "somewhere else" is often the market you're currently invested in.

2️⃣ Hot U.S. Jobs Data & Rate Hike Fears

The second major reason was the surprisingly strong U.S. employment data.

Reports suggested the U.S. economy added 172,000 jobs, while expectations were around 88,000, almost double the forecast.

This immediately changed the market's expectations. Strong employment data means the economy is still running hot, making it harder for the Federal Reserve to justify rate cuts. Instead, the possibility of further rate hikes gained momentum, with probabilities jumping from roughly 25% to 60%.

This pushed both the DXY (U.S. Dollar Index) and Treasury yields higher.

Historically, a strong DXY is one of the biggest headwinds for global financial markets. Even more importantly, whenever the U.S. 10-Year Treasury Yield remains above 4.5% while maintaining a bullish structure, financial markets tend to experience stress and liquidity pressure.

This is not a new narrative for me.

Since last year, I have repeatedly stated since last year that the market could eventually face a scenario where rates stay elevated and could hike for much longer than we expect. Persistent inflation, resilient economic data, rising energy prices, and geopolitical uncertainty have consistently supported that view.

Now, with a new Fed Chairman brought in by Trump, his key meeting scheduled within the next 10 days, elevated inflation concerns, double hot jobs data, high oil prices, and ongoing geopolitical tensions while the U.S. remains involved in global conflicts, investors simply do not know what comes next.

And when uncertainty rises, investors reduce risk.

Historically, Bitcoin and crypto are often among the first assets sold during risk-off events.

3️⃣ Cracks Starting to Appear in the AI Trade

The third major reason is that cracks are beginning to emerge in the AI trade.

Despite strong reports, Broadcom Inc. suffered a 15% decline, marking one of its worst performances of the year. The primary reason was simple: investors expected the company to raise its future revenue targets aggressively, and that didn't happen.

That single disappointment was enough to shake confidence across the entire AI space.

Broadcom's weakness quickly spread to other AI-related names, including NVIDIA, as investors started asking a very uncomfortable question:

"Are we paying too much simply because something has AI attached to its name?"

105

29

7

Monqoloid:Staying on sidelines; risk-off vibes make me wait.

Tadikif:If the Fed leans hawkish again, does that mean crypto stays under pressure until cuts resume, or can we see a liquidity rotation back to equities?

See all comments

View post details

🚨 WARNING: MONDAY COULD BE THE WORST MOMENT OF 2026!!

Make sure to take a look at this before June 8, that’s tomorrow.

The $SPCX IPO is coming on June 12.

And markets open this Monday, June 8.

This is the first real trading week before one of the biggest IPO events in market history.

SpaceX is expected to go public at around $1.75 TRILLION to $2 TRILLION valuation.

That one number explains everything.

Because money does NOT appear from nowhere.

If funds want to buy $SPCX, they need cash.

And where does that cash come from?

They sell what they already own.

Stocks will dump.

Crypto will dump.

High beta tech will dump even harder.

This is NOT just an IPO.

This is a liquidity drain.

Everyone sees the Elon hype.

Almost nobody sees the forced selling.

There are only a few ways this goes from here, and they are NOT equal.

- LIGHT SHOCK: funds sell small positions, stocks get hit first, crypto follows, then markets try to stabilize.

- HEAVIER SCENARIO: funds raise cash before June 12, high beta tech dumps, Bitcoin loses support, and retail gets trapped.

- WORST CASE: everyone rushes into $SPCX at the same time, liquidity disappears from crowded trades, stocks dump HARD, crypto gets hit first, and people get liquidated.

That last one is the REAL danger.

Because none of this is happening in a vacuum.

Stocks are already crowded.

Crypto is already weak.

Liquidity is already getting worse.

And now one of the most hyped IPOs in history is about to absorb even more money.

Now connect the dots.

If everyone wants $SPCX, they need dollars.

To get dollars, they sell assets.

And when everyone sells at the same time, markets do NOT dip slowly.

They dump.

This is NOT a theory.

The $SPCX IPO is June 12.

Markets open Monday, June 8.

And this is when positioning starts.

Markets are NOT pricing the liquidity drain now.

But they will.

I usually do the opposite of what the masses are doing.

Reminder: I’ve called all the market tops and bottoms for the last 15 years, including the Bitcoin bottom at $16,000 and the top at $126,000.

The next call will be even more important.

When I exit the markets completely, I’ll post it here publicly like I always do.

Turn notifications on. If you’re not following yet, you’ll understand why that was a mistake later.

Make sure to take a look at this before June 8, that’s tomorrow.

The $SPCX IPO is coming on June 12.

And markets open this Monday, June 8.

This is the first real trading week before one of the biggest IPO events in market history.

SpaceX is expected to go public at around $1.75 TRILLION to $2 TRILLION valuation.

That one number explains everything.

Because money does NOT appear from nowhere.

If funds want to buy $SPCX, they need cash.

And where does that cash come from?

They sell what they already own.

Stocks will dump.

Crypto will dump.

High beta tech will dump even harder.

This is NOT just an IPO.

This is a liquidity drain.

Everyone sees the Elon hype.

Almost nobody sees the forced selling.

There are only a few ways this goes from here, and they are NOT equal.

- LIGHT SHOCK: funds sell small positions, stocks get hit first, crypto follows, then markets try to stabilize.

- HEAVIER SCENARIO: funds raise cash before June 12, high beta tech dumps, Bitcoin loses support, and retail gets trapped.

- WORST CASE: everyone rushes into $SPCX at the same time, liquidity disappears from crowded trades, stocks dump HARD, crypto gets hit first, and people get liquidated.

That last one is the REAL danger.

Because none of this is happening in a vacuum.

Stocks are already crowded.

Crypto is already weak.

Liquidity is already getting worse.

And now one of the most hyped IPOs in history is about to absorb even more money.

Now connect the dots.

If everyone wants $SPCX, they need dollars.

To get dollars, they sell assets.

And when everyone sells at the same time, markets do NOT dip slowly.

They dump.

This is NOT a theory.

The $SPCX IPO is June 12.

Markets open Monday, June 8.

And this is when positioning starts.

Markets are NOT pricing the liquidity drain now.

But they will.

I usually do the opposite of what the masses are doing.

Reminder: I’ve called all the market tops and bottoms for the last 15 years, including the Bitcoin bottom at $16,000 and the top at $126,000.

The next call will be even more important.

When I exit the markets completely, I’ll post it here publicly like I always do.

Turn notifications on. If you’re not following yet, you’ll understand why that was a mistake later.

23

7

1

Medivacs_are_OP:Feels like hype, not a real liquidity shock.

Assistantothe:Are we sure funds will actually sell, or just rotate?

See all comments

View post details

After shrugging off $AVGO -12.6% on Thursday, the strong jobs report drove the 2yr yld +10bps to the highest levels since early 2025 & S&P -2.6% on Fri. For the wk, S&P/Nas/SOXX/Mag7 were -2.6%/-4.7%/-4.7%/-5.8% despite oil -3% to $91.

This is what I posted on X on last Sunday night “Over the near-term, the overall market at some point will need to take a breather from increasingly overbought technical conditions. After nine straight weekly gains, the S&P is now up 19% from its recent closing low on March 30th. But I feel like any losses will be contained to the typical ~5% pullback which is typically seen three to four times per year.”

After being up for nine straight weeks, the S&P went from an all-time closing high on Tuesday June 2nd and 14-day RSI of 75 to an RSI of 49 on Friday June 5th and down 3.0% from that Tuesday level.

During the internet infrastructure buildout between December 31, 1994 and the peak on March 10, 2000, the S&P tripled, the Nasdaq went up 6.7x and the SOXX Index advanced 9.5x. The S&P during this time had its 14-day RSI cross below 70 (overbought level) fifty times. 36% of the time, that day was the low point before it crossed back above 70 again. 42% of the time the low was reached within 2 trading days and 62% within three days. The average was 10 trading days to hit a short-term low and down 2.5% on average from the overbought level before the advance started to the next overbought reading.

Next week, there will be several potential market moving events. The $AAPL WWDC is on Monday. With the stock price surge into this event, a sell the news reaction would not be surprising much like with recent tech results. But I am bullish longer-term given after a 2 year wait we should finally get an AI infused iPhone. I am also very bullish on the larger form factor of a foldable phone that has driven major upgrade cycles in the past. Samsung introduced a foldable in 2019.

CPI on Wednesday will be closely watched along with how bond yields react. $ORCL results are also that day which should be solid given recent commentary from major customer OpenAI as well as related hyper-scaler cloud results. Having said that, a new CFO may want to set very achievable initial FY27 guidance that could disappoint.

The ECB is likely to raise rates on Thursday since being on hold after cutting rates in June of 2025 to 2.0%. Commentary will likely set the bar for the Fed in the following week.

Over the long-term I remain bullish given: 1) S&P earnings are expected to increase 25% this year driven by the advent of Agentic AI, 2) I believe oil prices will come down to the $80ish level given the political toll it is extracting on the US administration every day that the Strait of Hormuz is closed, and 3) new Fed Chairman Warsh is likely to push back against calls to raise rates. I view this recent pullback as well needed to work off the recent froth versus marking "the top."

All the best in the week ahead.

This is what I posted on X on last Sunday night “Over the near-term, the overall market at some point will need to take a breather from increasingly overbought technical conditions. After nine straight weekly gains, the S&P is now up 19% from its recent closing low on March 30th. But I feel like any losses will be contained to the typical ~5% pullback which is typically seen three to four times per year.”

After being up for nine straight weeks, the S&P went from an all-time closing high on Tuesday June 2nd and 14-day RSI of 75 to an RSI of 49 on Friday June 5th and down 3.0% from that Tuesday level.

During the internet infrastructure buildout between December 31, 1994 and the peak on March 10, 2000, the S&P tripled, the Nasdaq went up 6.7x and the SOXX Index advanced 9.5x. The S&P during this time had its 14-day RSI cross below 70 (overbought level) fifty times. 36% of the time, that day was the low point before it crossed back above 70 again. 42% of the time the low was reached within 2 trading days and 62% within three days. The average was 10 trading days to hit a short-term low and down 2.5% on average from the overbought level before the advance started to the next overbought reading.

Next week, there will be several potential market moving events. The $AAPL WWDC is on Monday. With the stock price surge into this event, a sell the news reaction would not be surprising much like with recent tech results. But I am bullish longer-term given after a 2 year wait we should finally get an AI infused iPhone. I am also very bullish on the larger form factor of a foldable phone that has driven major upgrade cycles in the past. Samsung introduced a foldable in 2019.

CPI on Wednesday will be closely watched along with how bond yields react. $ORCL results are also that day which should be solid given recent commentary from major customer OpenAI as well as related hyper-scaler cloud results. Having said that, a new CFO may want to set very achievable initial FY27 guidance that could disappoint.

The ECB is likely to raise rates on Thursday since being on hold after cutting rates in June of 2025 to 2.0%. Commentary will likely set the bar for the Fed in the following week.

Over the long-term I remain bullish given: 1) S&P earnings are expected to increase 25% this year driven by the advent of Agentic AI, 2) I believe oil prices will come down to the $80ish level given the political toll it is extracting on the US administration every day that the Strait of Hormuz is closed, and 3) new Fed Chairman Warsh is likely to push back against calls to raise rates. I view this recent pullback as well needed to work off the recent froth versus marking "the top."

All the best in the week ahead.

57

14

7

007ggman:S&P -2.6% on Friday, 2y yield +10bps, RSI 49 from 75; weekly losses averaging ~5% post-9-week streak, consistent with prior overbought pullbacks.

pellosanto:Feels heavy; I’ll wait for a cleaner bounce.

See all comments

View post details

$SPACZZX.P I mentioned "trillions in revenue by 2035 and 2040" but no one shared a solid plan. If every AI company is guessing same growth, will our GDP double by 2030...like growing 10-15% yearly for five years just to match AI alone...but that's not the whole economy. It's national GDP, not one company. I'm confused. $TSLA $MU $SOXX Let's figure this out

37

9

4

RaucetheSoss:Feels like everyone’s chasing AI hype, but the actual plans seem sketchy. I’m cautiously optimistic, not convinced.

See all comments

View post details

$ARKK -$MSTR For penny stocks, check out Alpha Compute (ALP). Around a 6 million market cap, it's an AI infrastructure firm focused on GPUaaS and confidential computing, using NVIDIA Blackwell GPU clusters. Recently bought a 60% stake in GAMEE from Animoca Brands. Their setup supports Telegram’s Cocoon AI network. They’ve got a 32.2 million dollar contract, with a 7.5 million upfront payment. When all data centers are ready by September, they expect 72 million in yearly revenue. ALP trades at 0.41 NTM sales compared to the peer average of 11.85x, even with early AI compute revenue signs (https://finance.yahoo.com/sectors/technology/articles/alpha-compute-21-million-ntm-154912417.html). It's heavily shorted now. Only 11.93 million free float. DD

13

4

Share

howardkitty94:Everyone cheering the cheap multiple, but what if ALP’s revenue is soft and the short squeeze fades once Blackwell ramps?

IllustratorSquare377:Big picture: ALP’s 60% stake in GAMEE and Telegram ties it to a niche but growing AI-native ecosystem. The 32m contract and 7.5m upfront look solid, yet the tiny float and heavy shorts suggest volatility, not value.

See all comments

View post details

$INTC They can! And don't call me Shirley! LOL!

Like

Comment

Share

26

4

2

Jelopuddinpop:I’m new here and kinda confused. If AI spending is “messed up everywhere,” why are SPY and NVDA still up? Doesn’t that sound like a bubble? Are we just chasing CNBC headlines instead of fundamentals?

Puzzleheaded-Mood544:Feels like we’re riding a froth train. Excited, but the AI hype feels stretched after 10 weeks of SPY gains.

See all comments

68

17

5

Traglc:Rates still higher; how sustainable is this rally?

TheMegabot:Seen this movie before: late-cycle pops, then chop. I remember 2013 and 2018 chasing winners. Diversify, stay patient, and avoid overpaying.

See all comments

View post details

$NVDA not rushing. It'll happen when nobody's watching.

10

Comment

1

View post details

My Pre-Market Bullish Watchlist for 6/9 (Daily Timeframe) $IREN: Many people are excited about $IREN, especially after it dropped recently and supports AI companies with data centers and power. "iren is down 13%. They provide the data centers and power distribution for AI companies." $NOW: Some folks are looking at $NOW, hoping for a dip to buy more. "I had a great run with $NOW, sold and bought again." $MU: Micron Technology is expected to do well with its earnings coming up. "MU is still going up with earnings on 6/24" Buy the Dip: Traders are eyeing recent market drops. "Pretty much anything. After the sell off this week I'm sure we will see a big rally next week" High Volatility and Volume: Good daily and weekly trading often involves stocks with high volatility, high volume, and news events. "stop thinking in terms of “best stocks” and think in terms of high volatility + high volume + news catalysts."

Like

Comment

Share

49

16

4

mayorolivia:Basically, the market is split on AI momentum: some see strong cash flows, others worry about valuation and growth slowing. Until earnings show direction, it feels like choppy risk-on/off trading.

See all comments

View post details

$LTCUSDT no need to overthink just go for it

15

4

1

Alex09464367:Feels like a buy-the-dip vibe right now.

ZhangtheGreat:I'm not convinced this is a sustainable setup. Liquidity's thin, correlation to BTC is near 1, and volumes look fragile. Without a real catalyst or chart confirmation, chasing 'just go for it' feels premature.

See all comments

View post details

$SPY Which industries and stocks will be affected to support SpaceX, OpenAI, and Anthropic's IPOs

8

Comment

Share

View post details

U.S. stock futures dipped Monday night after Israel and Iran paused their attacks, reducing tensions. Semiconductor stocks bounced back from last week's losses, boosting investor mood, though everyone's still watching the U.S. inflation numbers due Wednesday. Wall Street ended mixed, with the Nasdaq gaining from chipmakers, the S&P 500 rising slightly, and the Dow dropping due to worries about the Middle East's economic impact. Markets are also paying attention to the Strait of Hormuz, where ongoing issues keep oil prices high and inflation fears alive. Investors are waiting for May CPI data to see if rising fuel costs and shipping problems are pushing inflation up, after last week's strong jobs report. $SPY $QQQ $DIA $NVDA $SOXX

38

11

5

Steric-Repulsion:So basically, the ceasefire eased the Middle East jitters, so chip stocks popped, but we’re still nervous about CPI and oil. Nasdaq up, S&P up a bit, Dow down because of the region’s economic impact.

See all comments

View post details

🚨 TODAY: Apple $AAPL closed 1.9% lower at $301.54 after unveiling a long-delayed Siri AI overhaul at WWDC, per Reuters. https://t.co/EvlmEDx8Rv

91

25

7

goldeneye700:Feels like a classic tech cycle moment: AI hype, then a stumble. With rates still sticky and growth cooling, AAPL’s stumble makes sense.

free_loader_3000:If Siri’s overhaul is real, why did AAPL miss the target? Are we overestimating incremental impact on margins and revenue?

See all comments

Like

Comment

Share

View post details

$CRM full circle back I'm stepping away better places to park money Market isn't trusting the AI agentic story and honestly neither am I We've seen 100s of new AI agentic companies in the past 6 months and it's becoming a commodity which is very concerning Headcount licensing is also under threat I no longer see the risk reward here and I may be wrong but Salesforce will be around for a long time but the stock might be stuck for a long time GL

Like

Comment

Share

Like

Comment

Share

View post details

American Airlines Group, Inc. ($AAL) SpicyTrade - Daily Stock Analysis https://youtu.be/Wg1HQTZhwvU?si=l01lLD4v008iUC3U

12

Comment

1

View post details

$TSLA JP Morgan was wrong about Tesla, like we all knew. Now they're in a mess. "JPMorgan drops sell rating on Tesla after years, says it's leading in physical AI"

17

5

2

View post details

iShares Russell 2000 Index Fund ($IWM) SpicyTrade - Daily Stock Analysis https://youtu.be/gPW0UmFFckQ?si=03XWsltfaB6SZSPi

Like

Comment

Share

No More Posts

Disclaimer: The above is a summary showing certain market information. AInvest is not responsible for any data errors, omissions or other information that may be displayed incorrectly as the data is derived from various resources. Communications displaying market prices, data and other information available in this post are meant for purely informational purposes and are not intended as an offer or solicitation for the purchase or sale of any security. Please do your own research or consult a professional before making investment decisions. Keep in mind that past performance of any security or financial product does not guarantee future returns.Report an Issue

CONTACT US

Email: support@ainvest.com

Address: 330 7th Ave, Suite 902, New York, NY 10001, US

Copyright 2026 AInvest Fintech Inc. All rights reserved.