The right question isn't "is AVGO cheap at $430?" It's "is the custom silicon moat still intact — and who is most likely to erode it?"

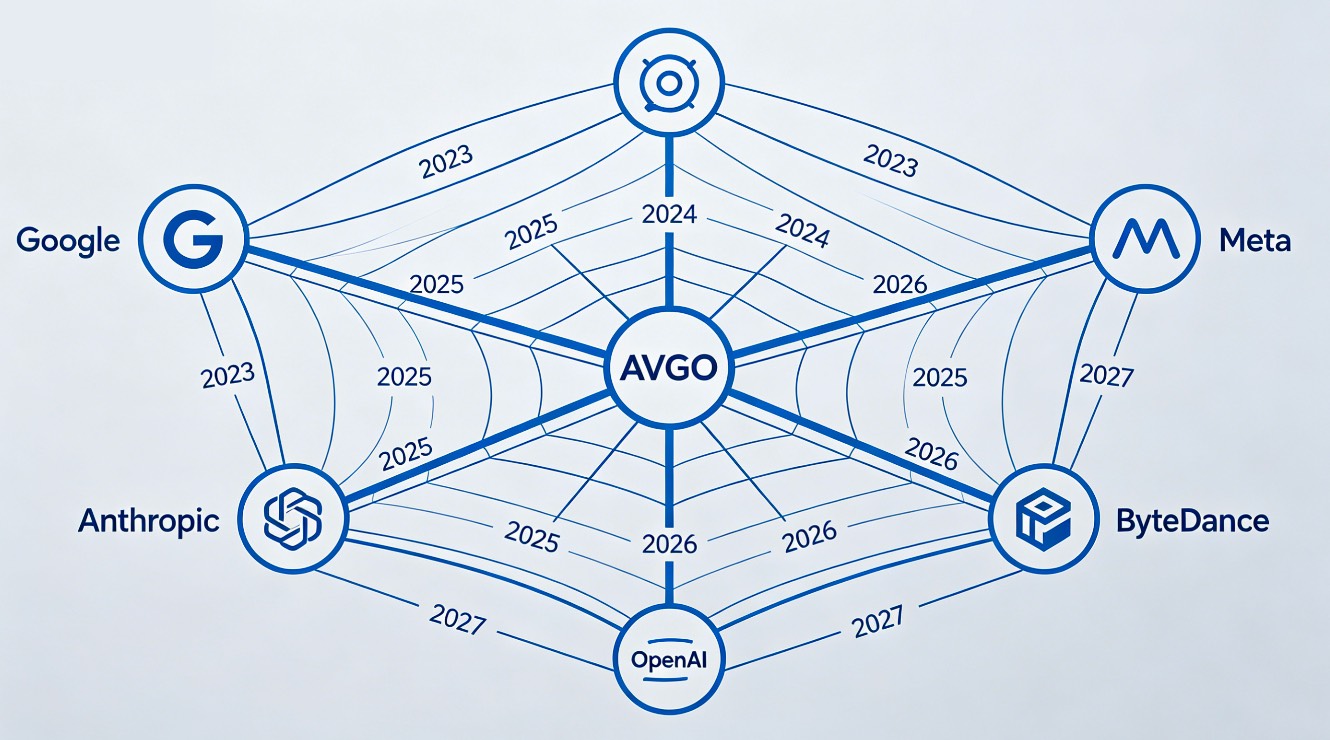

Let's be precise about the moat. Broadcom's business model is fundamentally different from Nvidia's. Nvidia sells the same H100/B200 to everyone. Broadcom co-designs a unique XPU for each hyperscaler client — Google's TPU, Meta's MTIA, ByteDance's internal silicon, and now chips for Anthropic and OpenAI. Each design takes 18–24 months of co-engineering. Once the chip is in production, the customer can't switch without losing 2 years of development time and rebuilding from scratch. That's an extraordinarily high switching cost.

The moat is real. But it has three genuine vulnerabilities.

First: insourcing risk. Amazon already moved Trainium 3 fully in-house. Microsoft is deepening Maia 2 without Broadcom involvement. If Meta or Google decides to follow AWS and build its own networking + accelerator stack entirely, Broadcom loses a customer representing 15–20% of revenue with no replacement pipeline.

Second: concentration. Five customers represent roughly 50% of Broadcom's semiconductor revenue. That's not a diversified business — it's a concentrated bet on the continued AI capex commitments of five specific companies. If any one of them hits a capex cycle pause, the impact is immediate and disproportionate.

Third: the software miss this week. Infrastructure software — the VMware/enterprise stack — came in $140M light. That's 0.6% of revenue. But the trend matters more than the number. If software is plateauing while AI chips soar, the "AI + software compounding" re-rating thesis loses one of its two legs.

The bull case survives all three of these risks — for now. Google's supply agreement runs through 2031. Meta's MTIA roadmap still relies on Broadcom networking even if compute moves in-house. Anthropic and OpenAI are new customers adding to the revenue base. And the Q3 guide of $16B at 200% YoY growth is, by any measure, extraordinary.

But at 87x earnings, "survives the risks" isn't enough. You need "dominates despite the risks." That's a different standard. And that's why today's NFP — and whether it gives AVGO a multiple-expansion tailwind from rate relief — matters as much as the fundamental story.

Volatility like this is where I park cash and watch AVGO. If NFP softens and rates ease, I’ll nibble on dips, but I’m hedging with a small NVDA collar. The moat’s there, just not bulletproof.

The multiple here is hostage to the labor market and rates. If NFP stays soft into summer, the Fed might pause, and AVGO could get a tailwind. But if capex slows, even a 10% drop in hyperscaler spend hits margins fast.

At 87x forward and 16B guide, the math doesn’t scream “buy.” Software off $140M, revenue mix still heavy on hyperscalers. If AWS Trainium and MSFT Maia 2 accelerate, what’s the margin cushion if one customer pauses capex?

Every dollar goes toward buying back $HYPE from the market and burning it.

That's why $HYPE keeps hitting new all-time highs even when the broader market is bleeding

Hard to feel bullish when BTC is down and liquidity tightens; $HYPE ATHs on buybacks feel fragile until macro stabilizes.

Watching from sidelines; if buybacks keep flowing and burns are real, I might nibble, but this feels like hype over substance.

Everyone’s calling this a dump, but what if liquidity dries up first? Could a small bid actually push it higher?

Feels hot; I’ll scalp it, not chase.

Trend looks strong if it holds above the recent swing high; I’m leaning into momentum until it stalls. Watching BTC correlation and volume. If it keeps ripping, I’ll add; otherwise, I’ll fade the pop.

Ok here me out. Earnings were so strong but they were looking for a massive raise due to raised AI demand but they had reported AI demand remains explosive, AI revenue beat own forecast, Q3 revenue expected to reach $16BN, over 200%+ YoY growth.

Broadcom is also up 70%+ in the last 2 months so lets be fair... it was a bit overbought for such a giant. I believe this dip right to the 34MA will shape up for the next leg up through summer & fall for 550.

My thesis hasn't change. It's a matter of building a base in the same range where it was just lastweek

Buy the dip to 34MA, or wait for Broadcom?

Everyone’s cheering the beat, but the stock was already frothy; feels like classic AI hype chasing itself.

Everyone’s cheering AI demand, but I’m skeptical this isn’t just optics-driven euphoria. Guidance raises often precede pullbacks. If Broadcom’s already overbought, why assume AVGO is immune? Market’s pricing perfection, not probabilities.

Tempting, but I’m staying cautious on HYPERUSDT.

Feels like the market’s signaling strong interest in HYPERUSDT, probably riding BTC’s momentum. If BTC holds highs, HYPERUSDT could keep chasing. But if BTC cools, this pair likely fades fast.

Looks like a pump, but spreads and liquidity look thin. If BTC wobbles, HYPERUSDT could gap hard. Watching order book depth.

Looks like a rug pull waiting to happen.

Feels like the HYPERUSDT pump is real and getting juicier. If BTC momentum holds and USDT liquidity stays tight, this could keep ripping. I’m riding the wave, but I’m watching for a pullback before adding.

I’m not convinced this is sustainable. Without real utility, adoption, and stable listings, the hype fades fast. Where’s the roadmap and traction?

Nobody’s talking about the $100B+ Treasury supply hitting the market this week.

Liquidity doesn’t care about your

So basically, Treasury sales mean less cash, which could cap rallies. But is that actually happening this week, or just a headline scare?

Higher yields from supply will pressure growth names.

I’m on the sidelines watching how the supply hits. If yields spike, I’ll wait for a flush in NVDA; if liquidity stays soft, I’ll nibble MSFT instead.

🇺🇸 1999: Berkshire's cash hit record highs before the dot-com crash. Nasdaq fell 78%.

2007: Cash climbed to fresh highs before the 2008 crash. S&P 500 dropped 57%.

2019: Cash reached $128,000,000,000 before the COVID crash.

2026: Cash at $397,400,000,000. Triple the 2019 peak.

13 consecutive quarters of net stock sales.

$172,930,000,000 in equities sold 2022-2024.

The patient capital isn't predicting.

It's preparing.

So basically, Warren’s selling stocks to pile up cash, and history says that often precedes downturns—does that mean we’re bracing for another drop?

Kinda weird to see cash at record levels again. Feels like the market’s bracing, but I’m nervous and tempted to overreact.

Funny how every time cash hits a record, everyone panics. It’s not a crystal ball. If you’re selling stocks to build cash, maybe you’re not buying the right ones. Feels like confirmation bias dressed up as wisdom.

Micron

The demand behind those earnings is not inventory restocking. HBM capacity is sold out through 2026 with price and volume locked under long term agreements, three suppliers control over 95 percent of global DRAM, and meaningful capacity expansion is unlikely until late 2027 or 2028. That is not a commodity. That is an oligopoly selling an input with no substitute into the largest capex wave in technology history.

An 8x multiple says the market is still underwriting the 2018 glut. The cyclical reputation is exactly why the market refuses to grant a full valuation, but the mix shift into high margin AI memory is structural, not a spot spike that mean reverts. Price the durability of contracted earnings rather than the reflex of past cycles and the stock is not expensive, it is mispriced.

The cycle has been rewritten for

Is MU still the momentum leader in memory?

MU up ~700% but forward multiple ~8x vs. sector ~37x; HBM sold out through 2026, DRAM oligopoly tight. Feels like valuation lag.

MU looks heavy; I’m fading strength into resistance.

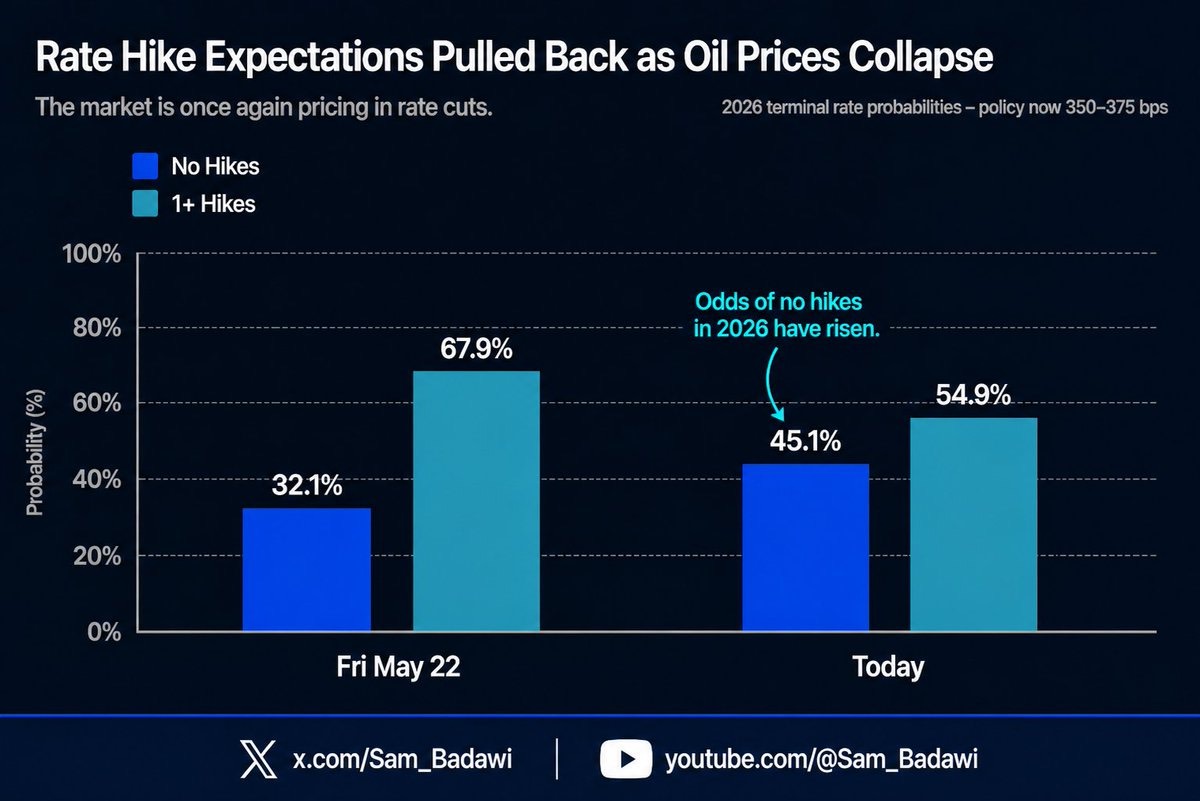

crude oil prices are reducing one of the market's biggest inflation concerns, which could allow rate cuts to get priced back into expectations.

The market has already started shifting, with the probability of no rate hikes for 2026 rising from 32.1% to 45.1%, while the odds of one or more hikes have fallen from 67.9% to 54.9%.

Markets love a headline shift, then forget the next week.

So basically oil dropping makes rate-cut odds look better, but I’m not convinced that’s sustainable without demand proof.

Oil softening and a higher no-hike probability for 2026 feels like a relief for balance sheets, but I’m watching refiners like VLO and MPC for margin stability, and energy names like XOM for dividend resilience.