Community/NVDA

AInvest curates key KOL insights on NVDA.

View post details

The selloff last week revealed something important about how the market prices different types of AI exposure — and why the rotation from hardware to software could be both inevitable and violent.

Hardware AI (Nvidia, Broadcom, AMD, Micron) is a capex cycle bet. You're essentially betting that hyperscalers continue spending $50–60B per quarter on AI infrastructure indefinitely. The thesis is simple and powerful when rates are low: borrow cheap, build fast, the ROI comes later. When rates spike — as they did Friday with the 10Y hitting 4.54% — the "ROI comes later" part becomes a problem. Higher discount rates make future cash flows worth less. Hardware AI stocks get hit hardest because their earnings are largely front-loaded (the spending is happening now) while the monetization is still uncertain.

Software AI (Apple, Salesforce, ServiceNow, Microsoft) is a monetization cycle bet. You're betting that AI features drive incremental revenue — higher prices, lower churn, more seats, new services. The multiple is lower (40-60x vs 80-90x for hardware), but so is the sensitivity to rates. More importantly, software AI doesn't require the customer to keep spending on infrastructure. Once the AI feature is in the product, the revenue recurs.

The irony: the market spent six months rotating INTO hardware AI because the ROI story was clearer. Now, with rates rising and hardware stocks repricing, the rotation is reversing. Software AI — which looked boring compared to Nvidia's vertical chart — suddenly looks like the safer bet.

Apple sits at the intersection. 2.2 billion devices is the distribution advantage no hyperscaler can match. If Siri 2.0 drives even a 5% increase in services revenue, that's $5B+ in high-margin, recurring revenue that doesn't require a data center to scale.

Today's WWDC is the first real test of whether the rotation from hardware AI to software AI is real — or just a wishful narrative.

Hardware AI (Nvidia, Broadcom, AMD, Micron) is a capex cycle bet. You're essentially betting that hyperscalers continue spending $50–60B per quarter on AI infrastructure indefinitely. The thesis is simple and powerful when rates are low: borrow cheap, build fast, the ROI comes later. When rates spike — as they did Friday with the 10Y hitting 4.54% — the "ROI comes later" part becomes a problem. Higher discount rates make future cash flows worth less. Hardware AI stocks get hit hardest because their earnings are largely front-loaded (the spending is happening now) while the monetization is still uncertain.

Software AI (Apple, Salesforce, ServiceNow, Microsoft) is a monetization cycle bet. You're betting that AI features drive incremental revenue — higher prices, lower churn, more seats, new services. The multiple is lower (40-60x vs 80-90x for hardware), but so is the sensitivity to rates. More importantly, software AI doesn't require the customer to keep spending on infrastructure. Once the AI feature is in the product, the revenue recurs.

The irony: the market spent six months rotating INTO hardware AI because the ROI story was clearer. Now, with rates rising and hardware stocks repricing, the rotation is reversing. Software AI — which looked boring compared to Nvidia's vertical chart — suddenly looks like the safer bet.

Apple sits at the intersection. 2.2 billion devices is the distribution advantage no hyperscaler can match. If Siri 2.0 drives even a 5% increase in services revenue, that's $5B+ in high-margin, recurring revenue that doesn't require a data center to scale.

Today's WWDC is the first real test of whether the rotation from hardware AI to software AI is real — or just a wishful narrative.

78

23

5

TeslaCoin1000000:I’m trimming speculative hardware and increasing software weight. Keeping cash for dips; if rates stay sticky, recurring AI revenue feels like the safer portfolio position.

therealchengarang:Volatility like this is where I nibble. If NVDA keeps selling out, I’ll add; if MSFT/AAPL show real AI stickiness, I’ll rotate.

See all comments

View post details

Part 1: (What's the next move for Crypto and Stocks)

Friday, 5th June 2026, was one of the worst days for financial markets in the past 12 months. Nearly $2.5 trillion got wiped out in a single day. Stocks crashed hard, crypto and

$BTC

got hit, commodities dropped, $OIL weakened, $XAU sold off, and panic spread across almost every asset class. It is very rare to witness such a broad-based selloff where virtually everything gets sold together.

After digging much deeper into it, I came to understand that there were three major reasons behind this move.

1️⃣ The Mega IPO Liquidity Drain

The market has three massive upcoming IPOs on the horizon: $SpaceX, $OpenAI, and $Anthropic, carrying a combined valuation of around $4 trillion.

Now think about it for a moment. How will the funding for these offerings come from retail and institutional investors? Money doesn't magically appear. Large investors need liquidity, and liquidity is often raised by selling existing positions. Money never leaves the financial markets, it just rotates.

According to Business Insider reports, SpaceX and other IPO candidates will not be fast-tracked into the S&P 500 after all, but that doesn't change the fact that investors have been preparing for these listings. SpaceX alone is expected to raise approximately $75 billion, making it one of the largest IPO events in history.

When opportunities of this size emerge, money gets pulled from somewhere else. That "somewhere else" is often the market you're currently invested in.

2️⃣ Hot U.S. Jobs Data & Rate Hike Fears

The second major reason was the surprisingly strong U.S. employment data.

Reports suggested the U.S. economy added 172,000 jobs, while expectations were around 88,000, almost double the forecast.

This immediately changed the market's expectations. Strong employment data means the economy is still running hot, making it harder for the Federal Reserve to justify rate cuts. Instead, the possibility of further rate hikes gained momentum, with probabilities jumping from roughly 25% to 60%.

This pushed both the DXY (U.S. Dollar Index) and Treasury yields higher.

Historically, a strong DXY is one of the biggest headwinds for global financial markets. Even more importantly, whenever the U.S. 10-Year Treasury Yield remains above 4.5% while maintaining a bullish structure, financial markets tend to experience stress and liquidity pressure.

This is not a new narrative for me.

Since last year, I have repeatedly stated since last year that the market could eventually face a scenario where rates stay elevated and could hike for much longer than we expect. Persistent inflation, resilient economic data, rising energy prices, and geopolitical uncertainty have consistently supported that view.

Now, with a new Fed Chairman brought in by Trump, his key meeting scheduled within the next 10 days, elevated inflation concerns, double hot jobs data, high oil prices, and ongoing geopolitical tensions while the U.S. remains involved in global conflicts, investors simply do not know what comes next.

And when uncertainty rises, investors reduce risk.

Historically, Bitcoin and crypto are often among the first assets sold during risk-off events.

3️⃣ Cracks Starting to Appear in the AI Trade

The third major reason is that cracks are beginning to emerge in the AI trade.

Despite strong reports, Broadcom Inc. suffered a 15% decline, marking one of its worst performances of the year. The primary reason was simple: investors expected the company to raise its future revenue targets aggressively, and that didn't happen.

That single disappointment was enough to shake confidence across the entire AI space.

Broadcom's weakness quickly spread to other AI-related names, including NVIDIA, as investors started asking a very uncomfortable question:

"Are we paying too much simply because something has AI attached to its name?"

Friday, 5th June 2026, was one of the worst days for financial markets in the past 12 months. Nearly $2.5 trillion got wiped out in a single day. Stocks crashed hard, crypto and

$BTC

got hit, commodities dropped, $OIL weakened, $XAU sold off, and panic spread across almost every asset class. It is very rare to witness such a broad-based selloff where virtually everything gets sold together.

After digging much deeper into it, I came to understand that there were three major reasons behind this move.

1️⃣ The Mega IPO Liquidity Drain

The market has three massive upcoming IPOs on the horizon: $SpaceX, $OpenAI, and $Anthropic, carrying a combined valuation of around $4 trillion.

Now think about it for a moment. How will the funding for these offerings come from retail and institutional investors? Money doesn't magically appear. Large investors need liquidity, and liquidity is often raised by selling existing positions. Money never leaves the financial markets, it just rotates.

According to Business Insider reports, SpaceX and other IPO candidates will not be fast-tracked into the S&P 500 after all, but that doesn't change the fact that investors have been preparing for these listings. SpaceX alone is expected to raise approximately $75 billion, making it one of the largest IPO events in history.

When opportunities of this size emerge, money gets pulled from somewhere else. That "somewhere else" is often the market you're currently invested in.

2️⃣ Hot U.S. Jobs Data & Rate Hike Fears

The second major reason was the surprisingly strong U.S. employment data.

Reports suggested the U.S. economy added 172,000 jobs, while expectations were around 88,000, almost double the forecast.

This immediately changed the market's expectations. Strong employment data means the economy is still running hot, making it harder for the Federal Reserve to justify rate cuts. Instead, the possibility of further rate hikes gained momentum, with probabilities jumping from roughly 25% to 60%.

This pushed both the DXY (U.S. Dollar Index) and Treasury yields higher.

Historically, a strong DXY is one of the biggest headwinds for global financial markets. Even more importantly, whenever the U.S. 10-Year Treasury Yield remains above 4.5% while maintaining a bullish structure, financial markets tend to experience stress and liquidity pressure.

This is not a new narrative for me.

Since last year, I have repeatedly stated since last year that the market could eventually face a scenario where rates stay elevated and could hike for much longer than we expect. Persistent inflation, resilient economic data, rising energy prices, and geopolitical uncertainty have consistently supported that view.

Now, with a new Fed Chairman brought in by Trump, his key meeting scheduled within the next 10 days, elevated inflation concerns, double hot jobs data, high oil prices, and ongoing geopolitical tensions while the U.S. remains involved in global conflicts, investors simply do not know what comes next.

And when uncertainty rises, investors reduce risk.

Historically, Bitcoin and crypto are often among the first assets sold during risk-off events.

3️⃣ Cracks Starting to Appear in the AI Trade

The third major reason is that cracks are beginning to emerge in the AI trade.

Despite strong reports, Broadcom Inc. suffered a 15% decline, marking one of its worst performances of the year. The primary reason was simple: investors expected the company to raise its future revenue targets aggressively, and that didn't happen.

That single disappointment was enough to shake confidence across the entire AI space.

Broadcom's weakness quickly spread to other AI-related names, including NVIDIA, as investors started asking a very uncomfortable question:

"Are we paying too much simply because something has AI attached to its name?"

105

29

7

Monqoloid:Staying on sidelines; risk-off vibes make me wait.

Tadikif:If the Fed leans hawkish again, does that mean crypto stays under pressure until cuts resume, or can we see a liquidity rotation back to equities?

See all comments

View post details

Everyone is debating whether to buy AVGO on the dip. Most of them are asking the wrong question.

The right question isn't "is AVGO cheap at $430?" It's "is the custom silicon moat still intact — and who is most likely to erode it?"

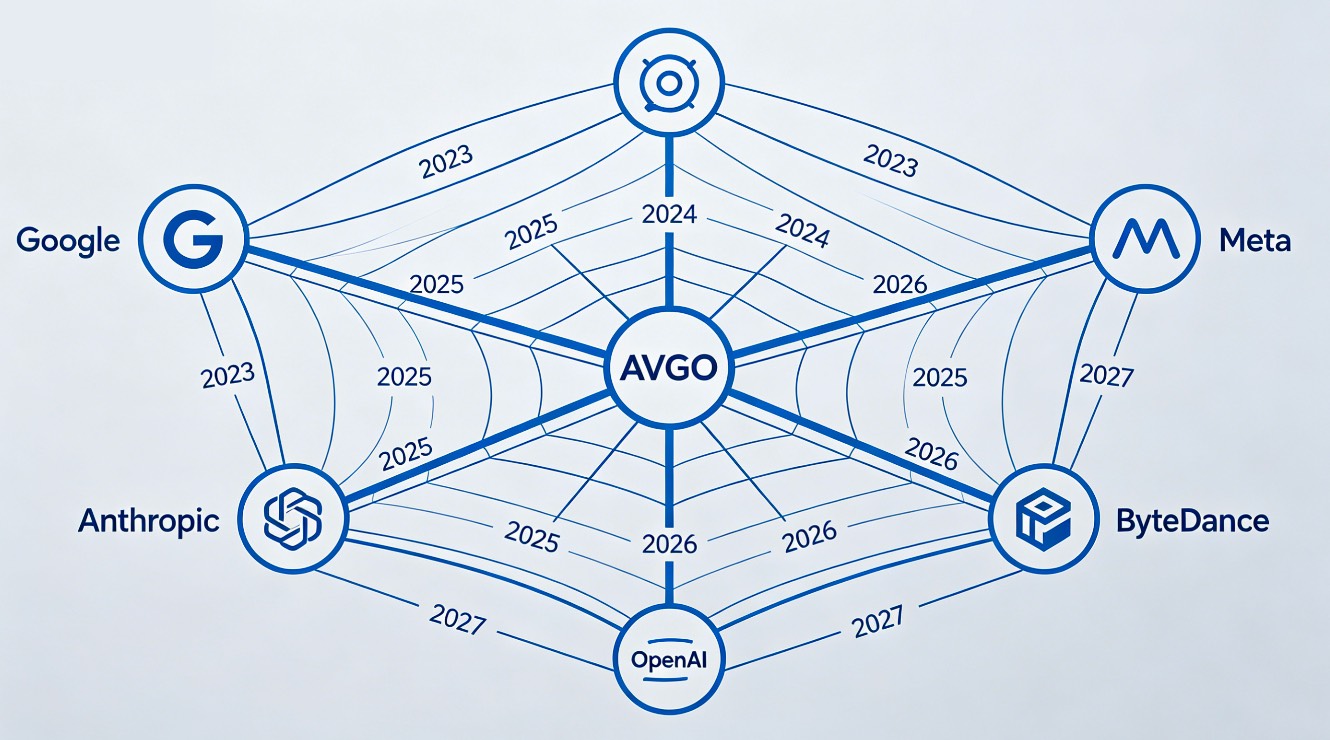

Let's be precise about the moat. Broadcom's business model is fundamentally different from Nvidia's. Nvidia sells the same H100/B200 to everyone. Broadcom co-designs a unique XPU for each hyperscaler client — Google's TPU, Meta's MTIA, ByteDance's internal silicon, and now chips for Anthropic and OpenAI. Each design takes 18–24 months of co-engineering. Once the chip is in production, the customer can't switch without losing 2 years of development time and rebuilding from scratch. That's an extraordinarily high switching cost.

The moat is real. But it has three genuine vulnerabilities.

First: insourcing risk. Amazon already moved Trainium 3 fully in-house. Microsoft is deepening Maia 2 without Broadcom involvement. If Meta or Google decides to follow AWS and build its own networking + accelerator stack entirely, Broadcom loses a customer representing 15–20% of revenue with no replacement pipeline.

Second: concentration. Five customers represent roughly 50% of Broadcom's semiconductor revenue. That's not a diversified business — it's a concentrated bet on the continued AI capex commitments of five specific companies. If any one of them hits a capex cycle pause, the impact is immediate and disproportionate.

Third: the software miss this week. Infrastructure software — the VMware/enterprise stack — came in $140M light. That's 0.6% of revenue. But the trend matters more than the number. If software is plateauing while AI chips soar, the "AI + software compounding" re-rating thesis loses one of its two legs.

The bull case survives all three of these risks — for now. Google's supply agreement runs through 2031. Meta's MTIA roadmap still relies on Broadcom networking even if compute moves in-house. Anthropic and OpenAI are new customers adding to the revenue base. And the Q3 guide of $16B at 200% YoY growth is, by any measure, extraordinary.

But at 87x earnings, "survives the risks" isn't enough. You need "dominates despite the risks." That's a different standard. And that's why today's NFP — and whether it gives AVGO a multiple-expansion tailwind from rate relief — matters as much as the fundamental story.

The right question isn't "is AVGO cheap at $430?" It's "is the custom silicon moat still intact — and who is most likely to erode it?"

Let's be precise about the moat. Broadcom's business model is fundamentally different from Nvidia's. Nvidia sells the same H100/B200 to everyone. Broadcom co-designs a unique XPU for each hyperscaler client — Google's TPU, Meta's MTIA, ByteDance's internal silicon, and now chips for Anthropic and OpenAI. Each design takes 18–24 months of co-engineering. Once the chip is in production, the customer can't switch without losing 2 years of development time and rebuilding from scratch. That's an extraordinarily high switching cost.

The moat is real. But it has three genuine vulnerabilities.

First: insourcing risk. Amazon already moved Trainium 3 fully in-house. Microsoft is deepening Maia 2 without Broadcom involvement. If Meta or Google decides to follow AWS and build its own networking + accelerator stack entirely, Broadcom loses a customer representing 15–20% of revenue with no replacement pipeline.

Second: concentration. Five customers represent roughly 50% of Broadcom's semiconductor revenue. That's not a diversified business — it's a concentrated bet on the continued AI capex commitments of five specific companies. If any one of them hits a capex cycle pause, the impact is immediate and disproportionate.

Third: the software miss this week. Infrastructure software — the VMware/enterprise stack — came in $140M light. That's 0.6% of revenue. But the trend matters more than the number. If software is plateauing while AI chips soar, the "AI + software compounding" re-rating thesis loses one of its two legs.

The bull case survives all three of these risks — for now. Google's supply agreement runs through 2031. Meta's MTIA roadmap still relies on Broadcom networking even if compute moves in-house. Anthropic and OpenAI are new customers adding to the revenue base. And the Q3 guide of $16B at 200% YoY growth is, by any measure, extraordinary.

But at 87x earnings, "survives the risks" isn't enough. You need "dominates despite the risks." That's a different standard. And that's why today's NFP — and whether it gives AVGO a multiple-expansion tailwind from rate relief — matters as much as the fundamental story.

70

20

8

Empty_Somewhere_2135:Volatility like this is where I park cash and watch AVGO. If NFP softens and rates ease, I’ll nibble on dips, but I’m hedging with a small NVDA collar. The moat’s there, just not bulletproof.

car12703:The multiple here is hostage to the labor market and rates. If NFP stays soft into summer, the Fed might pause, and AVGO could get a tailwind. But if capex slows, even a 10% drop in hyperscaler spend hits margins fast.

See all comments

View post details

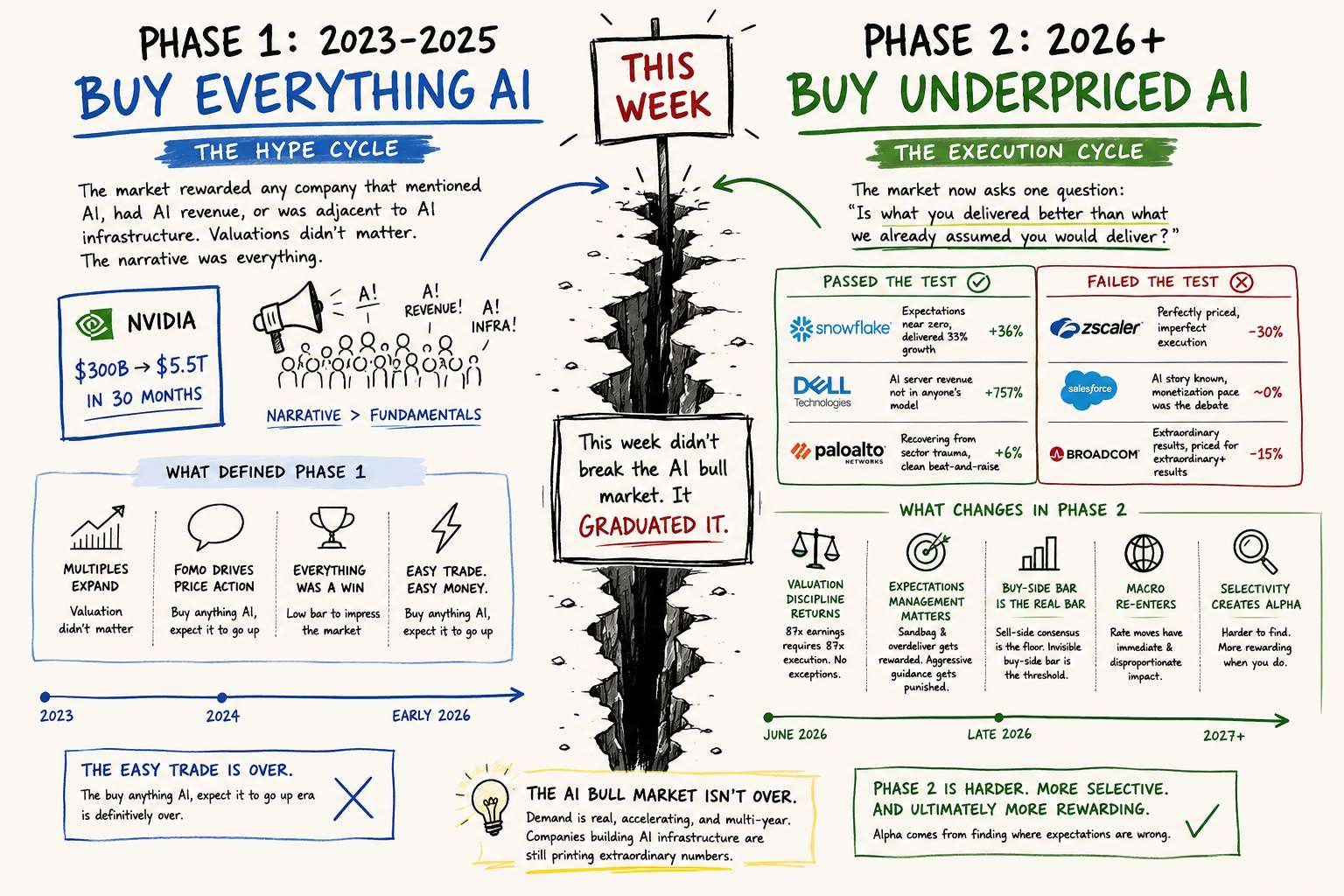

This week didn't break the AI bull market. It graduated it.

Phase 1 (2023–early 2026): The AI hype cycle. The market rewarded any company that mentioned AI, had AI revenue, or was adjacent to AI infrastructure. Valuations didn't matter. The narrative was everything. Nvidia going from $300B to $5.5T in 30 months is the defining data point of Phase 1.

Phase 2 (June 2026 onward): The execution cycle. Phase 1 ended not with a crash, but with a repricing. The market spent this week systematically repricing every major AI name based on one question: "Is what you delivered better than what we already assumed you would deliver?"

The companies that passed Phase 2's test: Snowflake (expectations near zero, delivered 33% growth), Dell (AI server revenue literally not in anyone's model at 757%), PANW (recovering from sector trauma, clean beat-and-raise).

The companies that failed Phase 2's test: Zscaler (perfectly priced, imperfect execution), Salesforce (AI story known, monetization pace was the debate), Broadcom (extraordinary results, but priced for extraordinary+ results).

What changes in Phase 2:

Valuation discipline returns. 87x earnings requires 87x execution. No exceptions.

Expectations management becomes a competitive advantage. The companies that sandbag guidance and overdeliver will be rewarded. The ones that set aggressive guidance will be punished on any shortfall.

The buy-side bar replaces earnings beats as the primary signal. Sell-side consensus is the floor. The invisible buy-side bar is the real threshold.

Macro re-enters the equation. In Phase 1, rate uncertainty was an inconvenience. In Phase 2, with multiples still extended, rate moves have immediate and disproportionate impact on stock prices.

The AI bull market isn't over. The companies building AI infrastructure are still printing extraordinary numbers. The demand is real, accelerating, and multi-year. But the easy trade — buy anything AI, expect it to go up — is definitively over.

Phase 2 is harder, more selective, and ultimately more rewarding for investors who do the work to find where expectations are wrong.

Welcome to the real AI trade.

Phase 1 (2023–early 2026): The AI hype cycle. The market rewarded any company that mentioned AI, had AI revenue, or was adjacent to AI infrastructure. Valuations didn't matter. The narrative was everything. Nvidia going from $300B to $5.5T in 30 months is the defining data point of Phase 1.

Phase 2 (June 2026 onward): The execution cycle. Phase 1 ended not with a crash, but with a repricing. The market spent this week systematically repricing every major AI name based on one question: "Is what you delivered better than what we already assumed you would deliver?"

The companies that passed Phase 2's test: Snowflake (expectations near zero, delivered 33% growth), Dell (AI server revenue literally not in anyone's model at 757%), PANW (recovering from sector trauma, clean beat-and-raise).

The companies that failed Phase 2's test: Zscaler (perfectly priced, imperfect execution), Salesforce (AI story known, monetization pace was the debate), Broadcom (extraordinary results, but priced for extraordinary+ results).

What changes in Phase 2:

Valuation discipline returns. 87x earnings requires 87x execution. No exceptions.

Expectations management becomes a competitive advantage. The companies that sandbag guidance and overdeliver will be rewarded. The ones that set aggressive guidance will be punished on any shortfall.

The buy-side bar replaces earnings beats as the primary signal. Sell-side consensus is the floor. The invisible buy-side bar is the real threshold.

Macro re-enters the equation. In Phase 1, rate uncertainty was an inconvenience. In Phase 2, with multiples still extended, rate moves have immediate and disproportionate impact on stock prices.

The AI bull market isn't over. The companies building AI infrastructure are still printing extraordinary numbers. The demand is real, accelerating, and multi-year. But the easy trade — buy anything AI, expect it to go up — is definitively over.

Phase 2 is harder, more selective, and ultimately more rewarding for investors who do the work to find where expectations are wrong.

Welcome to the real AI trade.

95

30

9

Sensitive-Fix8857:Feels like Phase 2 starts now. I’m watching SNOW and DELL for execution clarity before adding to my AI sleeve.

Wheremytendies:The math checks out: SNOW at 33% growth while expectations were near zero, DELL with 757% AI server revenue, PANW recovering. If multiples are disciplined, 87x requires consistency. I’m favoring SNOW and DELL over ZS and CRM until execution proves itself.

See all comments

View post details

Everyone is debating whether AVGO's selloff is a buying opportunity. Here's the question they should actually be asking: is the custom silicon model structurally defensible?

The answer is yes — but with one critical caveat. Custom chips like Broadcom's XPUs are co-engineered directly with the hyperscaler. Google's TPU isn't just "powered by Broadcom" — it's designed jointly, with roadmaps locked in years ahead. That creates switching costs that make AMD or even Nvidia almost irrelevant as competitors in this specific segment. The Google supply agreement reportedly runs through 2031.

The risk isn't competition. It's insourcing. Amazon already moved Trainium 3 fully in-house. Microsoft is deepening Maia 2. If Meta or ByteDance decides to follow, Broadcom loses a customer that represents 15–20% of revenue with no replacement on the shelf.

The selloff isn't telling you the thesis is broken. It's telling you the market finally started pricing that tail risk.

The answer is yes — but with one critical caveat. Custom chips like Broadcom's XPUs are co-engineered directly with the hyperscaler. Google's TPU isn't just "powered by Broadcom" — it's designed jointly, with roadmaps locked in years ahead. That creates switching costs that make AMD or even Nvidia almost irrelevant as competitors in this specific segment. The Google supply agreement reportedly runs through 2031.

The risk isn't competition. It's insourcing. Amazon already moved Trainium 3 fully in-house. Microsoft is deepening Maia 2. If Meta or ByteDance decides to follow, Broadcom loses a customer that represents 15–20% of revenue with no replacement on the shelf.

The selloff isn't telling you the thesis is broken. It's telling you the market finally started pricing that tail risk.

89

23

5

PatientPsy:Everyone assumes co-design equals monopoly; hyperscalers can pivot.

LonelyConely:Everyone cheering AVGO; I’m not convinced the risk is priced.

See all comments

View post details

The Trump administration just signed an executive order on AI innovation and security.

President's AI order is not just a chip headline...

These are the stocks I'm watching:

AI front-end: $NVDA $AMD $AVGO

Cloud: $MSFT $GOOGL $AMZN $ORCL

Data centers: $DELL $SMCI $VRT

Power/grid: $CEG $VST $ETN $PWR

Cybersecurity: $CRWD $PANW $ZS

Defense AI: $PLTR $BAH

The better question is what the order actually funds or removes friction from:

data center permitting

federal AI procurement

cyber/model security

power/grid buildout

AI exports

domestic semis

That is where the watchlist comes from.

President's AI order is not just a chip headline...

These are the stocks I'm watching:

AI front-end: $NVDA $AMD $AVGO

Cloud: $MSFT $GOOGL $AMZN $ORCL

Data centers: $DELL $SMCI $VRT

Power/grid: $CEG $VST $ETN $PWR

Cybersecurity: $CRWD $PANW $ZS

Defense AI: $PLTR $BAH

The better question is what the order actually funds or removes friction from:

data center permitting

federal AI procurement

cyber/model security

power/grid buildout

AI exports

domestic semis

That is where the watchlist comes from.

123

30

9

skilliard7:Still holding NVDA, but wary of policy-driven hype.

Chemical_Home6387:I’m on the sidelines, honestly. The list looks broad, but I’d rather see a concrete timeline or budget line item before touching any of these names. Feels exciting, but I’m not chasing.

See all comments

View post details

Up $3.4M in 2026 swing trading and $160,000+ for today only.

I've explained why these will explode BEFORE the crowd figures it out:

$NOW — Jensen Huang said agentic AI won't kill software companies. Best week since its 2012 IPO.

$IBM — Surged on Nvidia's new PC chip reveal + quantum AI hype. Trump call out.

$ARM — TD Cowen named its AGI CPU roadmap a secular demand inflection with

$MSFT

$AMD — Broad AI infrastructure buying wave; chip sector rally rips higher.

$INTC — 202% YTD return; Citi raised target citing AI inference server demand.

$ORCL — Stargate partner with OpenAI; $523B AI cloud backlog growing 438% YoY.

$AVGO— Custom AI chips rival Nvidia's GPUs; Q2 earnings drop June 3.

$HPE — Q2 earnings crushed expectations; revenue up 42% YoY, guidance raised.

$DELL — Record $113.5B revenue, $43B AI server backlog, $140B FY27 outlook.

$BE — Up 1,200%+ in a year; AI data centers need its off-grid power.

$KEEL— Canadian AI infrastructure corp trading alongside crypto/digital infrastructure peers in the AI data center buildout wave. Leopold call out.

The AI supercycle is only in Year 3 of 15. So we are still super early still. Be patient.

I've explained why these will explode BEFORE the crowd figures it out:

$NOW — Jensen Huang said agentic AI won't kill software companies. Best week since its 2012 IPO.

$IBM — Surged on Nvidia's new PC chip reveal + quantum AI hype. Trump call out.

$ARM — TD Cowen named its AGI CPU roadmap a secular demand inflection with

$MSFT

$AMD — Broad AI infrastructure buying wave; chip sector rally rips higher.

$INTC — 202% YTD return; Citi raised target citing AI inference server demand.

$ORCL — Stargate partner with OpenAI; $523B AI cloud backlog growing 438% YoY.

$AVGO— Custom AI chips rival Nvidia's GPUs; Q2 earnings drop June 3.

$HPE — Q2 earnings crushed expectations; revenue up 42% YoY, guidance raised.

$DELL — Record $113.5B revenue, $43B AI server backlog, $140B FY27 outlook.

$BE — Up 1,200%+ in a year; AI data centers need its off-grid power.

$KEEL— Canadian AI infrastructure corp trading alongside crypto/digital infrastructure peers in the AI data center buildout wave. Leopold call out.

The AI supercycle is only in Year 3 of 15. So we are still super early still. Be patient.

42

12

2

View post details

🚨 MICHAEL BURRY: S&P500 IS A BUBBLE

This guy solo predicted 2008 crash,

and made $800M for him and his investors.

Here's what he says now:

In 2024, Nvidia alone drove 33% of S&P 500 entire gain.

1 company. Out of 500.

And that's the revenue that made Nvidia worth $3+ trillion?

Michael Burry just called it "Fugazi."

SO THIS IS WHAT HAPPENED, AND I AM SHOCKED:

> Nvidia sold $5.4B worth of GPUs to a company called Valor

> Valor is a shell company with no operations, no products, no employees

Its only purpose: hold legal title to those chips

> Nvidia also invested $1.9B of its own money INTO Valor

> So Nvidia sold chips to a buyer it partially funded itself

> Then booked $5.4B as completed revenue

The chips are physically inside Elon Musk's xAI data center, running Grok.

But on paper? They belong to nobody real.

Now where did Valor get the money?

Apollo raised $3.5B in debt, packaged it into securities, sold it to Athene.

Athene sells retirement annuities to ordinary Americans.

Your grandparents' savings are funding Elon's AI cluster.

And they have no idea.

Athene's numbers:

> $103B in Level 3 assets (no observable market price)

> 16x leverage Based in Bermuda, outside US insurance regulation

Every step is technically legal. That's exactly what they said about mortgage-backed securities in 2006.

One company driving 1/3 of S&P 500 gains,

while people believe we are in the bull market.

This guy solo predicted 2008 crash,

and made $800M for him and his investors.

Here's what he says now:

In 2024, Nvidia alone drove 33% of S&P 500 entire gain.

1 company. Out of 500.

And that's the revenue that made Nvidia worth $3+ trillion?

Michael Burry just called it "Fugazi."

SO THIS IS WHAT HAPPENED, AND I AM SHOCKED:

> Nvidia sold $5.4B worth of GPUs to a company called Valor

> Valor is a shell company with no operations, no products, no employees

Its only purpose: hold legal title to those chips

> Nvidia also invested $1.9B of its own money INTO Valor

> So Nvidia sold chips to a buyer it partially funded itself

> Then booked $5.4B as completed revenue

The chips are physically inside Elon Musk's xAI data center, running Grok.

But on paper? They belong to nobody real.

Now where did Valor get the money?

Apollo raised $3.5B in debt, packaged it into securities, sold it to Athene.

Athene sells retirement annuities to ordinary Americans.

Your grandparents' savings are funding Elon's AI cluster.

And they have no idea.

Athene's numbers:

> $103B in Level 3 assets (no observable market price)

> 16x leverage Based in Bermuda, outside US insurance regulation

Every step is technically legal. That's exactly what they said about mortgage-backed securities in 2006.

One company driving 1/3 of S&P 500 gains,

while people believe we are in the bull market.

77

22

4

ConstructionOk6948:Funny how we celebrate innovation while letting banks and insurers off-ramp risk. If these structures fail, who bears the pain?

Easy-Reference-8189:I’m new here—what exactly is a shell company, and how does it affect the stock price? If Nvidia sold chips to a shell, does that mean the revenue isn’t real? How would that impact my portfolio?

See all comments

Like

Comment

Share

View post details

$NVDA not rushing. It'll happen when nobody's watching.

7

Comment

1

42

14

3

mayorolivia:Basically, the market is split on AI momentum: some see strong cash flows, others worry about valuation and growth slowing. Until earnings show direction, it feels like choppy risk-on/off trading.

See all comments

25

8

4

View post details

U.S. stock futures dipped Monday night after Israel and Iran paused their attacks, reducing tensions. Semiconductor stocks bounced back from last week's losses, boosting investor mood, though everyone's still watching the U.S. inflation numbers due Wednesday. Wall Street ended mixed, with the Nasdaq gaining from chipmakers, the S&P 500 rising slightly, and the Dow dropping due to worries about the Middle East's economic impact. Markets are also paying attention to the Strait of Hormuz, where ongoing issues keep oil prices high and inflation fears alive. Investors are waiting for May CPI data to see if rising fuel costs and shipping problems are pushing inflation up, after last week's strong jobs report. $SPY $QQQ $DIA $NVDA $SOXX

33

10

4

Steric-Repulsion:So basically, the ceasefire eased the Middle East jitters, so chip stocks popped, but we’re still nervous about CPI and oil. Nasdaq up, S&P up a bit, Dow down because of the region’s economic impact.

See all comments

34

9

4

ramdomwalk:I'm oddly calm. If panic spikes, liquidity kicks in and mean reversion bites. Might be a buying window.

Spiritual-Author1500:Are we sure this isn't just noise and whiplash?

See all comments

View post details

$QQQ the dip in $AAPL is all you need to know $NVDA didn't bounce back either

Like

Comment

Share

View post details

$NVDA Ready for 250?

25

8

4

Electrical_Love_3670:From a sector lens, NVDA 250 assumes near-term demand doesn’t wobble. But data center spend is capex-heavy and lags, while AMD and others keep innovating. If hyperscaler budgets tighten, the whole AI chip story could cool fast.

fatuousfatwa:I’m new here and kinda torn. If NVDA hits 250, does that mean AI chips are unstoppable? I’m nervous about volatility and not sure I can stomach it.

See all comments

View post details

$NVDA brightside non option day tomorrow likely $212-214

Like

Comment

Share

4

Comment

Share

38

11

4

Abe719:If this rally is really tied to NVDA’s 2026 cluster roadmap, how sustainable is it with higher rates, sticky inflation, and potential supply chain bottlenecks? Do we see a rotation from growth to AI hardware, or just noise?

pais_tropical:Another AI hype pop; fundamentals still look thin.

See all comments

Like

Comment

Share

View post details

$NVDA is overpriced. Too much market cap. Too much hype. Might hit 300 before I'm done with my job (I'm 25)

28

8

2

View post details

$SPY buying and selling puts today, loaded up on Apple puts (sold 80%), some Tesla and Nvidia puts too. Holding VIX calls from last Thursday. Went from down 4k to up 11k. So happy with it. Volatility 🤑🤑🤑🤑

26

8

2

No More Posts

Disclaimer: the above is a summary showing certain market information. Ainvest is not responsible for any data errors, omissions or other information that may be displayed incorrectly as the data is derived from a third party source. Communications displaying market prices, data and other information available in this post are meant for informational purposes only and are not intended as an offer or solicitation for the purchase or sale of any security. Please do your own research when investing, All investments involve risk and the past performance of a security, or financial product does not guarantee future results or returns. Keep in mind that while diversification may help spread risk it does not assure a profit, or protect against loss, in a down market.

Trending

Hot Topics

June 8 Daily Discussion: The AI Hardware Trade Just Broke. Can Apple's Software Story Save It?

NEW

494 Posts

Bitcoin Reclaims $63K as Weekend Rebound Tests Market Fear

HOT

112 Posts

June 5 Daily Discussion: Can Jobs Data Keep the AI Rally Alive?

1149 Posts

June 4 Daily Discussion: Broadcom Beat. Wall Street Still Sold.

267 Posts

Bitcoin Hits Two-Month Low as Liquidations Reach $1.1B

450 Posts

CONTACT US

Email: support@ainvest.com

Address: 330 7th Ave, Suite 902, New York, NY 10001, US

Copyright 2026 AInvest Fintech Inc. All rights reserved.